Real Estate Agents Rally to Stop Intro 360 at New York City Hall

By Manhattan Real Estate Tracker, June 12, 2024

Real estate agents and brokers came out this morning to City Hall in Downtown Manhattan today to rally against Intro 360 which would require only those who hire a real estate agent to the broker fee. While all commissions are negotiable, typically the broker fee for leasing an apartment is 15 percent of the first year’s rent. New York City is unlike any city in the country, Manhattan Real Estate Tracker strongly opposes Intro 360.

According to the co-sponsor of the measure, City Council member Chi Ossé, renters deposit $10,000 on average for a new home. One major expense he wants to eliminate is the mandatory broker fee. However, landlords will simply raise the rent and in the long run, the renter would have paid more in rent than if they paid a broker fee and received a lower starting rent.

Tenants claim that they had to pay the broker fee even though “they didn’t hire a broker.” When an agent markets an apartment for rent and a potential tenant inquires about it, it was the agent’s experience and knowledge of real estate and marketing that not only secured the exclusive listing but also generated the call. This work has value and in certain cases, the agent should be compensated by the renter.

Links to local online articles regarding today’s rally and Intro 360 from local New York television stations can be found below.

Manhattan Real Estate Tracker will be attending the rally at City Hall on Wednesday, June 12, 2024 to oppose Int. 360. This bill would stop real estate brokers and agents of a landlord from collecting a broker’s fee from a renter. All agents and brokers can attend to support the opposition of this bill.

The City Council states, “This bill would require an individual who is a representative or an agent of a property owner or a prospective tenant in a residential rental real estate transaction to collect fees charged in the transaction from the party employing the individual. The provisions of this bill would not impact the collection of fees by a landlord or property owner.”

Advance Estimates of U.S. Retail and Food Services

Advance estimates of U.S. retail and food services sales for April 2024, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $705.2 billion, virtually unchanged (±0.4 percent) from the previous month, but up 3.0 percent (±0.5 percent) above April 2023. Total sales for the February 2024 through April 2024 period were up 3.0 percent (±0.5 percent) from the same period a year ago. The February 2024 to March 2024 percent change was revised from up 0.7 percent (±0.5 percent) to up 0.6 percent (±0.1 percent).

Retail trade sales were virtually unchanged (±0.4 percent) from March 2024, but up 2.7 percent (±0.5 percent) above last year. Non-store retailers were up 7.5 percent (±1.6 percent) from last year, while food services and drinking places were up 5.5 percent (±2.1 percent) from April 2023.

Programs for regulating rent, known as rent control and rent stabilization, are in place in several communities around New York State. Rent regulation has two purposes: first, to shield tenants in privately held buildings from unlawful rent hikes; second, to enable building owners to maintain their properties while making a fair profit. Of the two rent regulation schemes, rent control is the more established one. It was first implemented in response to the housing scarcity that followed World War II and is typically applicable to structures built before 1947. In general, rent stabilization applies to apartments that were freed from rent control and buildings constructed after 1947 but before 1974. It also includes buildings that are eligible for tax incentives under J-51, 421-a, and 421-g. The apartments that are eligible for these tax benefit programs are determined by their own set of regulations.

Rent stabilization outside of New York City is also referred to as ETPA, or the Emergency Tenant Protection Act, and it’s legal in a few counties and places (see Fact Sheet #8). Rent stabilization can also apply to housing accommodations whose rentals are set by public benefit corporations, DHCR, and other government bodies, as outlined in the rent regulations.

Rent Stabilization In addition to limiting the amount of rent increases, rent stabilization offers tenants protections. Tenants are entitled to the provision of necessary services, the renewal of their leases, and are not subject to eviction unless there are legally permissible reasons. Tenants have the option to extend their leases for one or two more years. Tenants can use a number of forms developed by the Division of Housing and Community Renewal (DHCR) to make pertinent complaints. After serving the owner with the complaint and gathering evidence, DHCR must issue a formal order that is appealable.

DHCR has the authority to lower rent and impose civil penalties on the owner in cases when a tenant’s rights are infringed. Should you fail to maintain services, your rent may be lowered. If there is an overcharge, the DHCR may impose interest penalties or triple damages that must be paid by the tenant.

Rent Control Rent control restricts the amount of rent an apartment owner can charge as well as the owner’s ability to evict residents. Additionally, tenants are entitled to certain necessities. Since tenants are regarded as “statutory” tenants, owners are not obligated to provide renewal leases. Tenants can use a number of forms developed by DHCR to file pertinent concerns. After serving the owner with the complaint and gathering proof, DHCR is authorized to issue a written order that is appealable. Rents may be lowered and civil penalties may be imposed by DHCR on the owner in the event that a tenant’s rights are infringed. Reduced rent is a possibility if services are not kept up. When there is an overcharge, the DHCR may determine the legally collectible rent.

Please refer to an attorney for legal advice regarding your specific situation. Additional information can be found at the Department of Homes and Community Renewal.

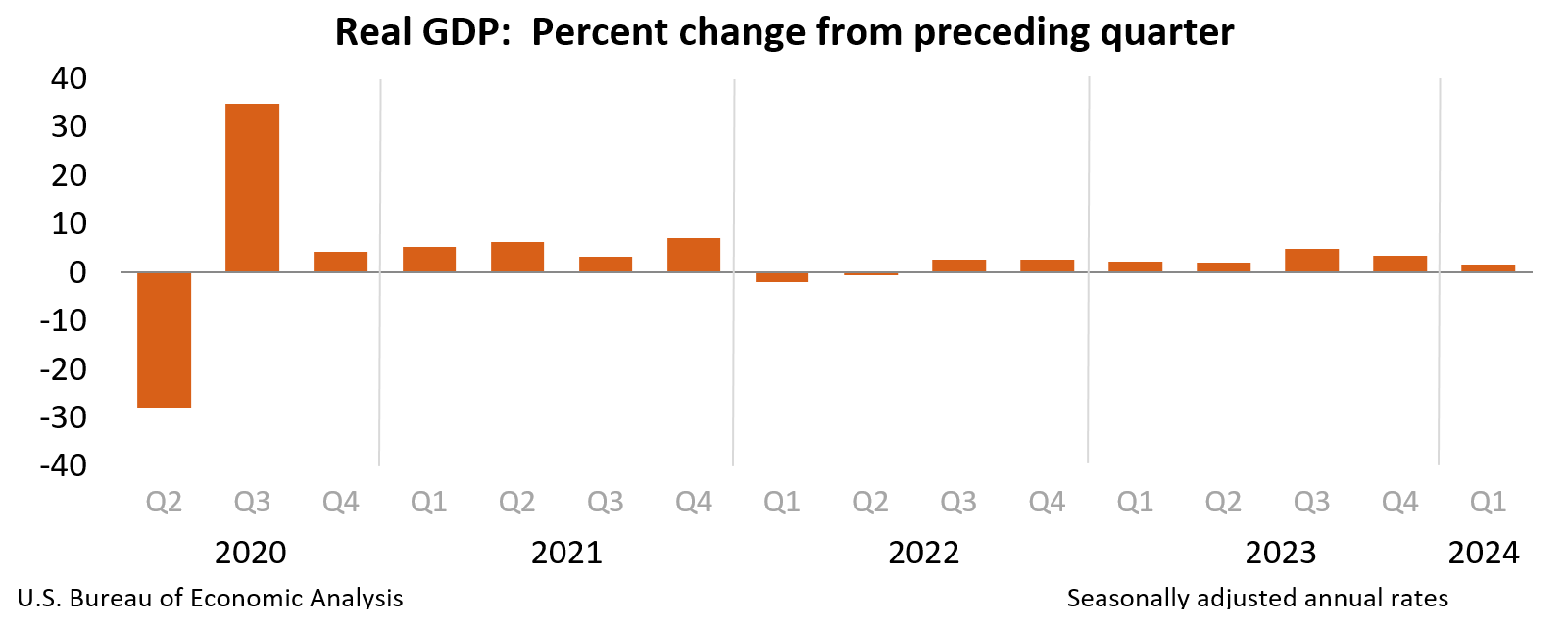

From the US Department of Commerce Bureau of Economic Analysis.

Real gross domestic product (GDP) increased at an annual rate of 1.6 percent in the first quarter of 2024 (table 1), according to the “advance” estimate released by the Bureau of Economic Analysis. In the fourth quarter of 2023, real GDP increased 3.4 percent.

The GDP estimate released today is based on source data that are incomplete or subject to further revision by the source agency (refer to “Source Data for the Advance Estimate” on page 3). The “second” estimate for the first quarter, based on more complete source data, will be released on May 30, 2024.

The increase in real GDP primarily reflected increases in consumer spending, residential fixed investment, nonresidential fixed investment, and state and local government spending that were partly offset by a decrease in private inventory investment. Imports, which are a subtraction in the calculation of GDP, increased (table 2).

The increase in consumer spending reflected an increase in services that was partly offset by a decrease in goods. Within services, the increase primarily reflected increases in health care as well as financial services and insurance. Within goods, the decrease primarily reflected decreases in motor vehicles and parts as well as gasoline and other energy goods. Within residential fixed investment, the increase was led by brokers’ commissions and other ownership transfer costs as well as new single-family housing construction. The increase in nonresidential fixed investment mainly reflected an increase in intellectual property products. The increase in state and local government spending reflected an increase in compensation of state and local government employees. The decrease in inventory investment primarily reflected decreases in wholesale trade and manufacturing. Within imports, the increase reflected increases in both goods and services.

Compared to the fourth quarter, the deceleration in real GDP in the first quarter primarily reflected decelerations in consumer spending, exports, and state and local government spending and a downturn in federal government spending. These movements were partly offset by an acceleration in residential fixed investment. Imports accelerated.

Current‑dollar GDP increased 4.8 percent at an annual rate, or $327.5 billion, in the first quarter to a level of $28.28 trillion. In the fourth quarter, GDP increased 5.1 percent, or $346.9 billion (tables 1 and 3).

The price index for gross domestic purchases increased 3.1 percent in the first quarter, compared with an increase of 1.9 percent in the fourth quarter (table 4). The personal consumption expenditures (PCE) price index increased 3.4 percent, compared with an increase of 1.8 percent. Excluding food and energy prices, the PCE price index increased 3.7 percent, compared with an increase of 2.0 percent.

Personal Income

Current-dollar personal income increased $407.1 billion in the first quarter, compared with an increase of $230.2 billion in the fourth quarter. The increase primarily reflected increases in compensation and personal current transfer receipts (table 8).

Disposable personal income increased $226.2 billion, or 4.5 percent, in the first quarter, compared with an increase of $190.4 billion, or 3.8 percent, in the fourth quarter. Increases in compensation and personal current transfer receipts were partly offset by an increase in personal current taxes, which are a subtraction in the calculation of DPI. Real disposable personal income increased 1.1 percent, compared with an increase of 2.0 percent.

Personal saving was $755.7 billion in the first quarter, compared with $815.5 billion in the fourth quarter. The personal saving rate—personal saving as a percentage of disposable personal income—was 3.6 percent in the first quarter, compared with 4.0 percent in the fourth quarter.

Source Data for the Advance Estimate

The GDP estimate released today is based on source data that are incomplete or subject to further revision by the source agency. Information on the source data and key assumptions used in the advance estimate is provided in a Technical Note and a detailed “Key Source Data and Assumptions” file posted with the release. The second estimate for the first quarter, based on more complete data, will be released on May 30, 2024. For information on updates to GDP, refer to the “Additional Information” section that follows.

* * *

Next release, May 30, 2024, at 8:30 a.m. EDT Gross Domestic Product (Second Estimate) Corporate Profits (Preliminary Estimate) First Quarter 2024

NEW YORK – New York City Mayor Eric Adams today released the City of New York’s balanced $111.6 billion Fiscal Year (FY) 2025 Executive Budget. Mayor Adams’ budget builds on the administration’s actions, since last fall, to stabilize the city’s fiscal outlook, and has positioned the city to backfill long-term programs that had only been funded with temporary stimulus funds while making the investments that double down on the city’s efforts to strengthen public safety, rebuild the economy, and make the city more livable. These investments will specifically add more police officers to city streets and subways, protect educational programs with city and recurring state funds and increase access to early childhood education, provide support for thousands of cultural institutions, and boost programs that improve the quality of life for working-class New Yorkers. By virtue of Mayor Adams’ strong fiscal management and better-than-expected revenue, the Adams administration balanced the budget, stabilized the city’s fiscal position and outlook, and prevented major service cuts, tax hikes, or layoffs.

FY24 and FY25 remain balanced, with outyear gaps of $5.5 billion, $5.5 billion, and $5.7 billion in Fiscal Years 2026 through 2028, respectively. Growth of $2.2 billion in FY25 over the Preliminary Budget is driven by stronger than expected economic activity in FY24 and an improved outlook in FY25.

“When we came into office two years ago, during the height of another wave of the COVID-19 pandemic, we were determined to protect public safety, rebuild our economy, and make our city more livable for working-class New Yorkers,” said Mayor Adams. “We have made great strides in these commitments, and today, crime is down, jobs are up, our streets are cleaners, we’re taking on major quality of life issues, and we have financed the most newly constructed affordable housing in a single year in our city’s history. Thanks to our strong fiscal management, we are able to invest in the things that matter to New Yorkers in this Fiscal Year 2025 Executive Budget, including public safety, early childhood education, and the needs of working-class people. As New York City moves toward the future, our core values will continue to guide us as we continue to build a safer, more equitable, and more prosperous city for all New Yorkers.”

Proactive Fiscal Management

On the heels of the pandemic, New York City had to confront substantial challenges, filling holes left where long-term programs were funded with temporary stimulus dollars, and the costs of funding fair labor deals that went years unresolved with city employees. While there are still reasons to remain cautious — like slowing revenue growth in coming fiscal years — by making smart decisions in the November and January plans — like monitoring spending and trimming agency and asylum seeker budgets — as well as better-than-expected revenue, the administration has balanced the budget and steadied the city’s fiscal position.

Strong and decisive action led to achieving a record level of gap-closing savings, and due to better-than-expected economic growth, the administration was able to cancel the previously announced Executive Budget Program to Eliminate the Gap (PEG). As good stewards of taxpayer dollars, the administration still achieved $41 million in agency expense savings, over FY24 and FY25, driven by underspending, where agencies spent less than expected to fund a program or service. This has no impact on service delivery.

Additionally, because continuing to fund the needs of the asylum seeker humanitarian crisis without any limits was not sustainable, Mayor Adams committed to PEG the city’s asylum seeker spending over FY24 and FY25 by a total of approximately 30 percent between the Preliminary and Executive Budgets. As a result of the administration’s policies — including providing 30 to 60 days of housing, legal support, intensified case management, and reducing per diem household costs — more than 65 percent of the asylum seekers who have come through the city’s intake centers have left the city’s care and taken the next steps in their journeys. The administration has successfully cut migrant costs in the Executive Budget by $586 million over FY24 and FY25. Along with $1.7 billion in migrant costs previously cut in the FY25 Preliminary Budget, this brings the two-year total migrant PEG savings achieved to nearly $2.3 billion.

Total savings — including the asylum seeker PEGs — achieved in FY24 and FY25 over the November, January, and April Financial Plans is now $7.2 billion.

Additionally, tax revenue has been revised up by $619 million in FY24 and $1.7 billion in FY25 compared with the Preliminary Budget due to better than anticipated economic performance in 2023 and an improved economic outlook in 2024. These additional revenues were used to help remain balanced in FY24 and FY25. However, tax revenue growth is expected to cool in upcoming fiscal years as the local economy slows, bolstering the fact that the city cannot rely exclusively on revenue growth to resolve fiscal challenges.

Maintaining budget reserves as a hedge against the unexpected is a critical part of the administration’s strong financial management strategy. The FY25 Executive Budget maintains a near-record level $8.2 billion in reserves, including $1.2 billion in the General Reserve, $4.8 billion in the Retiree Health Benefits Trust Fund, $250 million in the Capital Stabilization Reserve, and $1.96 billion in the Rainy-Day Fund.

FY25 Priorities

The FY25 Executive Budget enhances safety and doubles down on the Adams administration’s efforts to continue to bring down crime by adding two more police classes this year and putting 1,200 additional police officers on the streets by adding July and October New York City Police Department (NYPD) classes. Now, all police academy classes will be fully funded in 2024. This adds 2,400 new police officers to city streets in the coming year and puts New York City on the path to having a total of 35,000 uniformed officers protecting New Yorkers in the coming years.

The Adams administration’s strong fiscal management, combined with a stronger than anticipated economic performance in 2023, helped put the city in a position to fund a number of stimulus-funded long-term programs that could be backfilled with city and state dollars. In the FY25 Executive Budget, Mayor Adams uses $514 million in city and recurring state funds to support key education programs that had been funded with expiring stimulus dollars, including mental health care, career readiness, and literacy programs for New York City public school students.

More specifically, some highlighted investments of the FY25 Executive Budget include:

Keeping New Yorkers Safe

Doubling down on decreases in homicides and shootings by adding 1,200 more police recruits between the July and October NYPD classes, putting New York City on a path to have 35,000 uniformed officers in the coming years ($62.4 million, FY25).

Funding for the Job Connections initiative, which will connect 500 young New Yorkers at risk of gun violence with career readiness and green job placement programs ($16.9 million, FY25).

Expanding the Crisis Management System to support additional Cure Violence coverage areas and additional mental health services in gun violence safety precincts ($8.6 million, FY25).

Supporting the Neighborhood Safety Alliance, which fosters collaboration between communities, actors, law enforcement agencies, and city services to reduce gun violence in six additional precincts ($2.5 million, FY25).

Securing a Better Future for New York City Children

Supporting citywide 3-K expansion as it transitions from its original stimulus funding source ($92 million, FY25).

Supporting nearly 500 social workers and psychologists who provide mental health supports in schools ($74 million, FY25) *.

Maintaining funding for special education Pre-K providers to increase service hours, and resources for DOE-related services and evaluation teams ($56 million, FY25)*.

Investing in pathways programs that facilitate career pathways programs in high schools — offering apprenticeships, career-readiness, and access to college credits ($53 million, FY25)*.

Arts funding programming ($41 million, FY25).

Literacy and dyslexia programs and academic assessments for both English language arts, and math ($17 million, FY25)*.

Funding for coordinators for students in temporary housing in schools and shelters ($17 million, FY25)*.

Bilingual education funding for curriculum and assessment, teacher preparation and staffing, professional learning, and multilingual family and community engagement for 100 bilingual programs ($10 million, FY25)*.

Increasing the availability of in-school early childhood education classes and services for students with special needs ($25 million, FY25).

Maximizing enrollment in early childhood education programming and helping parents connect with Pre-K and 3-K seats with an extensive media outreach and marketing campaign ($3.5 million, FY25).

* Indicates funded with recurring state resources.

Investing in Cherished Cultural Institutions

Allocating funding for the Cultural Institutions Group, 34 cultural nonprofits operated on city-owned property ($5.4 million, FY25).

Investing in the Cultural Development Fund, which supports over 1,000 cultural nonprofits across the city ($2.2 million, FY25).

Putting More Money in the Pockets of Working-Class New Yorkers

Ensuring eligible New Yorkers learn about supportive city programs that are available to them and make accessing the resources easy and efficient via the NYC Benefits Access Initiative ($4.6 million, FY25).

Helping low-to moderate-income communities by funding grants to create and support new Small Business Improvement Districts and merchant associations ($5.3 million, FY25).

Establishing the NYC Future Fund that will make loans to Black, indigenous, and people of color-owned businesses with a focus on early-stage businesses ($2 million, FY25).

Climate Budgeting

Mayor Adams is taking a critical step towards making the city cleaner and greener over generations to come in his FY25 Executive Budget. New York City is the first big city in America, and among a small elite group of cities internationally, to implement climate budgeting, a system that integrates climate targets and considerations into the budget process to help achieve the city’s goals of net-zero greenhouse gas emissions and resiliency to climate threats. Critically, climate impact will now be one of the many factors that will be balanced when allocating the city’s limited resources to ensure resources are aligned with sustainability and resiliency needs. And — for the first time and moving forward — the Executive Budget will also include a Climate Budgeting publication that will include an analysis of the city’s new and ongoing climate investments and progress toward emissions goals.

The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.4 percent in March on a seasonally adjusted basis, the same increase as in February, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 3.5 percent before seasonal adjustment. The index for shelter rose in March, as did the index for gasoline. Combined, these two indexes contributed over half of the monthly increase in the index for all items. The energy index rose 1.1 percent over the month. The food index rose 0.1 percent in March. The food at home index was unchanged, while the food away from home index rose 0.3 percent over the month. The index for all items less food and energy rose 0.4 percent in March, as it did in each of the 2 preceding months. Indexes which increased in March include shelter, motor vehicle insurance, medical care, apparel, and personal care.

The indexes for used cars and trucks, recreation, and new vehicles were among those that decreased over the month. The all items index rose 3.5 percent for the 12 months ending March, a larger increase than the 3.2-percent increase for the 12 months ending February. The all items less food and energy index rose 3.8 percent over the last 12 months. The energy index increased 2.1 percent for the 12 months ending March, the first 12-month increase in that index since the period ending February 2023. The food index increased 2.2 percent over the last year.

Fewer condos sold in Manhattan last month than in February, despite an uptick in the luxury market, while buyers in Brooklyn signed contracts for five more units than last month.

“With [March] demand closely resembling that of the pre-pandemic period, we may see some normalization of the market as mortgage rates stabilize,” said Marketproof CEO Kael Goodman.

Citywide, deal volume rose by 7% month-over-month, continuing an upward trajectory for the fourth month

Total dollar volume rose 18% to $796M, the best month since June of 2023The luxury market saw a 26% increase in deal volume from last month and a 7% increase in dollar volume

While the March numbers are upbeat, they fall short of the March average during the pandemic recovery (2021-2023) and align more closely with pre-pandemic (2015-2019) numbers

The upward momentum continues for the fourth month, though at a more subdued pace. Deal volume rose 7% from 262 in February to 281 in March. Deal count in Manhattan and Brooklyn was essentially unchanged, but Queens saw an uptick of 57%. The surge in Queens is attributed to a batch of 23 contracts reported at 134-16 35th Avenue. Total dollar volume increased by 18% to $769M from $676M. The median price per square foot (PPSF) dipped slightly from $1,635 to $1,587, and the median price decreased by 7% from $1.62M to $1.5M. The drop in unit price and PPSF reflects a more significant share of the deal volume originating in Queens, a borough with more modestly priced units.

While March’s performance improved month over month, the deal volume represents a 56% decrease compared to the average of 439 deals per month during the pandemic recovery period from 2021 to 2023. The demand in March 2024 aligns more closely with the 289 average during the pre-pandemic period from 2015 to 2019.

Of the 281 deals citywide, 133 (-1%) were in Manhattan, 107 (+5%) were in Brooklyn, and 41 (+57%) were signed in Queens.

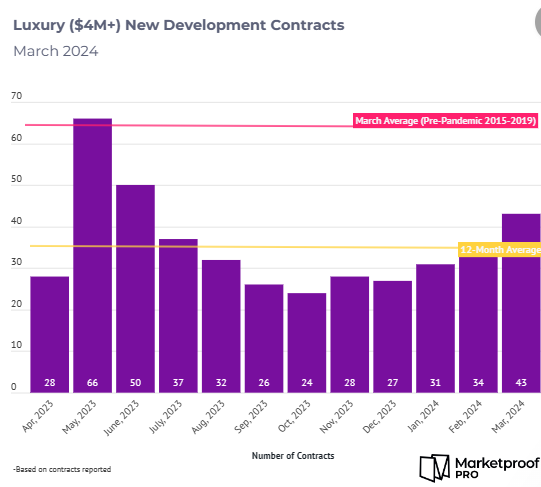

LUXURY

The luxury segment saw deal volume jump by 26% month over month, reaching a nine-month peak of 43 contracts. The total dollar volume grew by 42% from $300M to $427M. The median price rose 7% from $5.9M to $6.4M, and the median PPSF was unchanged at $2,631.

One High Line led in deal volume with six contracts over $4M. The West Chelsea complex found buyers for 95 of 235 residences since sales launched a little over a year ago. Corcoran Sunshine Marketing Group handles sales and marketing.

125 Perry Street led in dollar volume with three contracts totaling $112M, or 26% of the luxury market. The West Village boutique has sold 3 of the 7 residences. Compass handles sales and marketing.

Of the 43 luxury deals this month, 40 were in Manhattan, and three were signed in Brooklyn.

U.S. job growth was strong last month, and the unemployment rate fell slightly. But wage growth remained contained, underscoring the growing belief among economists and policymakers that the country can keep adding jobs without fanning inflation.

U.S. employers added a seasonally adjusted 303,000 jobs in March, the Labor Department reported on Friday, significantly more than the 200,000 economists expected. The unemployment rate slipped to 3.8%, versus February’s 3.9%, in line with expectations.

Average hourly earnings in March rose 0.3% from the previous month. That put them up 4.1% from a year earlier, marking the smallest on-the-year gain since June 2021.

Stocks edged up following the report, and Treasury yields moved higher.

Investors have been on edge recently over economic data suggesting that Federal Reserve interest-rate cuts might not be imminent. A stronger-than-expected labor market could feed into those concerns—first because increased spending power for consumers could fuel inflation, and second because a strong labor market gives the central bank more leeway to wait before cutting rates.

The Fed is mandated to keep employment as strong as possible while keeping inflation under control. Balancing those objectives has put the central bank in a difficult position as it mulls cutting interest rates this year: Cut too soon, or by too much, and inflation could heat back up all over again. Wait too long, and the strain of high rates could damage the job market, pushing the economy into a recession.

The labor market has continued to add jobs over the past year despite high interest rates. At the same time, the unemployment rate has drifted up and wage gains have cooled. In March of last year, the unemployment rate was 3.5%.

Those dynamics have defied the conventional wisdom that, for inflation to cool, job creation would need to dramatically slow down.

Lately many economists and even Fed officials have come to believe that, in part as a result of immigration, the supply of available workers has increased. If that is right, the number of jobs can grow faster.

Supply alone isn’t enough to generate job gains, however; there has to be demand. At the moment, it still looks as if there is plenty of that. Layoff activity remains low, and the number of unfilled jobs is high, with the Labor Department reporting earlier this week that there were 8.8 million job openings as of the end of February. The job-opening rate, or openings as a share of filled and unfilled positions, was 5.3%. That has fallen over the past year, but in prepandemic 2019—a period of strength for the job market—that ratio averaged 4.5%.

But the share of people quitting their jobs each month has fallen to prepandemic levels, which indicates that the intensity with which businesses were hiring away workers from each other has subsided. Moreover, the private-sector job market has been drawing most of its strength from just two broad sectors—private education and healthcare, and leisure and hospitality.

Private education and healthcare added 88,000 jobs last month, while leisure and hospitality added 49,000. Combined, the two have accounted for 1.5 million of the 2.9 million jobs the U.S. has gained in the past year.

Economists at Bank of America call those sectors “high touch.” Much of the work must be done in person, and a lot of it—such as waiting tables or working in a hospice—entails face-to-face interactions.

High-touch employment fell sharply when the pandemic hit, and even now, four years later, appears low. Relative to the trend during the five years before the pandemic, there are some two million fewer jobs in those sectors than might have been expected.

This raises a question, points out Bank of America economist Michael Gapen. “Should we expect employment in those sectors to return to their prior trend line? Or are there structural reasons to think maybe the employment gap will not close and therefore this catch-up effect could finish sooner?” he said.

He thinks the answer might be mixed. Lately, employment growth in leisure and hospitality has moderated. One reason why is that for some of those employers, business is still down—think restaurants near offices where many people are still working from home a few days a week. Another is that some businesses adopted practices when labor became short that probably won’t get undone. Lots of restaurants, for example, introduced QR codes in place of paper menus, allowing customers to place orders with their phones rather than waitstaff.

But for private education and healthcare, the story could be different. The loss of jobs these areas experienced when the pandemic hit was truly exceptional: Other than in 2020, employment in the sector has experienced near constant growth over the 85 years of available data. Moreover, the healthcare needs of an aging U.S. population will probably only grow. The sector is still about a million jobs short of its old trend. If that gap continues to narrow, as Gapen expects it will, it could help bolster job growth into next year.

NEW YORK — Five years after Albany Democrats overhauled the state’s rent-stabilization laws, real estate executives are looking to weaken the reforms — bolstered by data they commissioned that validates their case.

New findings from a survey of 781 property owners and managers covering about 242,000 units contend the 2019 changes led to disinvestment and substantial vacancies in rent-stabilized housing. A significant share of respondents said it is “economically infeasible” to invest in needed upgrades to their buildings. The study, obtained by POLITICO, was conducted by consulting firm HR&A Advisors on behalf of the Real Estate Board of New York and the Rent Stabilization Association. While the findings are unsurprising, real estate leaders are using them to fuel their argument against the 5-year-old legislative changes.

The issue is now entering the early stages of negotiations in Albany, amid broader discussions around a wide-ranging deal to tackle an acute housing shortage.

Tenant activists and progressive lawmakers are already pushing back on any attempt to reverse the reforms, which starts out as a tall order in the Democratic-led state Legislature.

“This data indicates that the 2019 rent law changes are having increasingly negative impacts on rent-stabilized apartments and tenants,” James Whelan, president of REBNY, said in a statement. “State lawmakers should follow the data and advance policies that facilitate the rehabilitation of dilapidated apartments in a manner that results in quality affordable housing without recreating the dynamics of vacancy decontrol.”

Real estate groups argue the 5-year-old changes — which eliminated or significantly curtailed avenues to raise rents on the city’s roughly 1 million rent-regulated apartments — have left landlords unable to rehab apartments and rerent them when long-term tenants move out.

The idea — called “self serving” by a leading tenant activist — has gained traction among some moderate Democrats: A bill introduced last year by state Sen. Leroy Comrie and Assemblymember Kenny Burgos would allow rent-stabilized landlords to reset rents at vacancy to facilitate renovations. The current law allows only very limited increases if an owner is making an apartment or building improvement.

Some prominent legislators see Comrie’s introduction as a non-starter and question the industry’s claims.

“They’re saying, let’s turn the rent-regulation system on its head because we have many units that are in dire disrepair — I don’t buy that,” said Assemblymember Linda Rosenthal, chair of the body’s housing committee. “Many of my colleagues oppose that vehemently, so I don’t think it will gain much traction, and it shouldn’t. This is not the time to be trying to undo tenant protections.”

The survey found that for owners with small portfolios that are primarily rent-stabilized — those under 11 units — 25 percent of their apartments are currently vacant.

There are also fewer total vacant apartments than there were in 2018, but longer-term vacancies — defined as three years or more — have increased, the REBNY-commissioned survey found. And nearly one-third of respondents cited “economic infeasibility” of unit improvements after a long tenancy as a reason for continued vacancies.

RSA supports the bill introduced by Comrie and Burgos. REBNY is not pushing that specific legislation but said it agrees with its general goals, and sees it as one potential approach.

“There’s no way to adjust rent at vacancy anymore in the rent-stabilized universe,” Basha Gerhards, senior vice president of planning at REBNY, said in reference to landlords’ reported drop in operating income. “So do we allow some form of rent reset in exchange for the apartments being improved and the violations being cleared? It’s a question we are posing.”

State lawmakers are under pressure to take action on housing issues this year as the city struggles with the lowest rental vacancy rate in 50 years and residential construction slows amidst the absence of a key multi-family housing tax break.

After Democrats took control of the chamber, they eliminated “vacancy decontrol” — a mechanism that allowed units to leave the rent-stabilization program when they reached a certain threshold and became vacant. They additionally got rid of a provision that permitted landlords to raise rents by 20 percent when apartments became vacant, and significantly restricted rent increases attached to building and apartment improvements.

Those provisions had led to the loss of tens of thousands of rent-regulated apartments before the 2019 reforms went into effect.

The survey found owners still need to make those upgrades — things like replacing boilers or kitchen appliances — but are pursuing fewer improvements since they no longer pencil out financially. For example, RSA members filed 763 individual apartment improvements in 2023, down from 3,311 in 2019. For individual apartment improvements, the maximum landlords can spend on renovations that would be eligible for a rent increase calculation is $15,000 over 15 years.

“Whether it’s big systems like rewiring or plumbing, or bringing [units] up to code, complying to lead paint regulations — that’s well over $15,000 for an apartment, so there’s just no incentive,” said Frank Ricci, an executive vice president at RSA.

The city’s Department of Housing Preservation and Development estimated last year there are only 2,500 low-cost apartments that are both in need of repairs and have been vacant for a year or more. The agency says that figure is significantly lower now, based on the latest housing and vacancy survey, though it has not yet released a specific number, according to Gothamist. Ricci argued smaller buildings are under-surveyed by the city survey.

“By and large, there are just not that many vacant rent-stabilized apartments in New York City right now,” said Cea Weaver, campaign coordinator for the Housing Justice for All coalition, pointing to HPD’s data. “It’s very politically convenient and self-serving to say, oh we’re in trouble because of the [2019 reforms.] But it’s like no, you’re in trouble because you speculated on buildings that are 100 years old and a pandemic happened and other costs changed.”

Weaver and other progressive activists said they’re nonetheless taking the push very seriously — and reject any attempts to include it in a broader housing agreement, even if that deal includes a longstanding priority known as “good cause” eviction. That measure would effectively limit rent hikes in market-rate apartments.

“For the left, we know what rollbacks have felt like — we experienced that in the bail reform fight,” said Jasmine Gripper, co-director of the Working Families Party. “We’ve been communicating to elected leaders that this is a non-starter.”