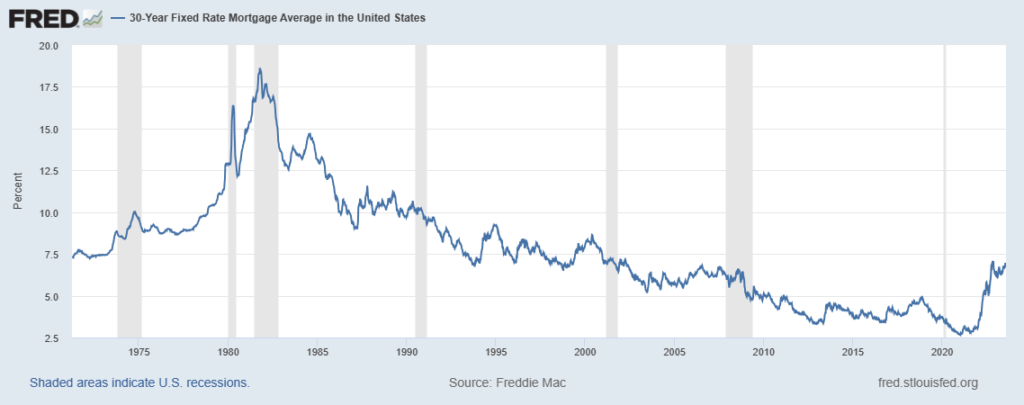

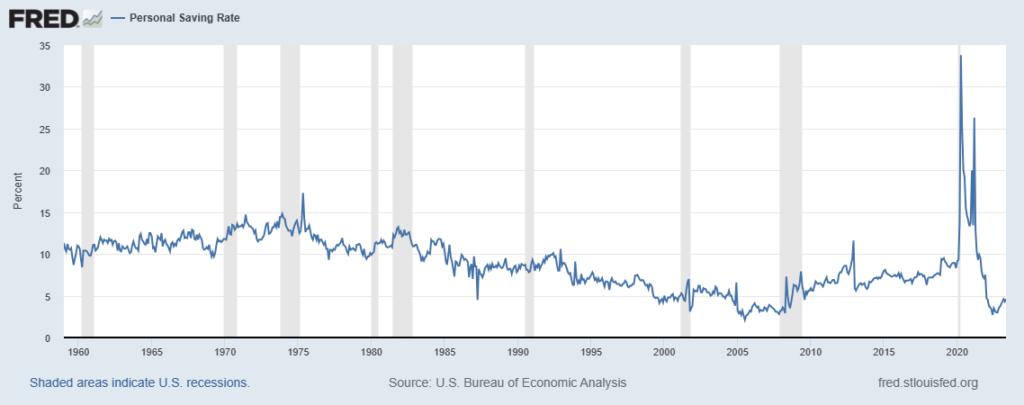

30 Year Fixed Rate Average Mortgage Rates and Average Personal Savings Each Year

From The Federal Reserve Bank of St. Louis Economic Data (FRED) :

Real Estate News, Information, Data and Insights for New York City Real Estate

From The Federal Reserve Bank of St. Louis Economic Data (FRED) :

From NY Post:

Downtown Manhattan is about to get a big dose of upstate New York.

Almost exactly two years after the Rochester-based grocery giant Wegmans announced it would debut its first-ever Manhattan location in the former Kmart on Astor Place during the second half of 2023, now comes word of its specific opening date. And, just like the company said in 2021, it’s right on target.

The two-level, 87,500-square-foot store — located in the 1907-built 770 Broadway — will open for business on Oct. 18 at 9 a.m., according to a company release.

It’s the first Wegmans location in Manhattan, but not the first within city limits.

“We know our customers can’t wait to come see what we have in store and our employees have been training, in some cases, for over a year to get ready for this day,” says store manager Matt Dailor in the release. “Wegmans is a celebration of food and people, and we can’t wait to open the doors on October 18 to our community here in the East Village.”

On Oct. 27, 2019, almost exactly four years before the opening of this Astor Place spread, Wegmans made its Big Apple debut across the East River in the Brooklyn Navy Yard, which remains open.

The bulk of Wegmans locations are in New York State — spanning from Buffalo to a forthcoming store in Long Island’s Suffolk County — with plenty of others in Pennsylvania, New Jersey, Massachusetts, Maryland, Delaware, the District of Columbia, Virginia and North Carolina. Future stores, according to the Wegmans website, will include one in Norwalk, Connecticut — which will be the first to open in that state.

The grand opening of the Astor Place behemoth comes full circle after summer 2021 saw speculation that Wegmans would move into the former Kmart, which shut abruptly in July 2021. Published reports, as well as Reddit chatter, said the space would be replaced by a “first-class regional grocer,” leading many curious minds to offer their guesses of Wegmans, Whole Foods or Trader Joe’s.

What customers can expect: fresh sushi, sandwiches, pizza and even Mediterranean bites from the “Mezze” section. What’s more, in the first half of 2024, visitors will also have an on-site dining room with a sushi bar, as well as a Champagne and oyster bar.

Similar to Trader Joe’s, Wegmans has long attracted a cult following — particularly among natives of Western and Central New York who grew up chowing down on its fresh, and reasonably priced, food.88

The loyalty was so strong for some upstate natives that, despite living in New York City, they’d drive 330 miles home to Rochester to load up on several months worth of groceries to cart back to Manhattan. Others deliberately rented apartments or bought homes near the closest Wegmans stores — and not just for breezy shopping, but also for nostalgia.

Longtime customer favorites include the brand’s ginger-flavored sparkling water, the cave-ripened Cremeux de Bourgogne cheese, chocolate-dipped chocolate chip cookies that sandwich flavored buttercream frosting and, this being an upstate brand, its Buffalo wings.

From NY Post:

A penthouse at 100 Vandam in downtown Manhattan has set a record for the highest publicized residential lease in New York City — renting for a jaw-dropping $125,000 per month.

The tenant has not been identified, but was represented by Platinum Properties agents Cyrus Eyn and Cash Bernard. Nest Seekers’ Jessica C. Campbell held the listing.

Occupying over 6,500 square feet, the duplex residence takes up the 20th and 21st floors of the 25-story building.

Made up of six bedrooms and seven bathrooms, the home boasts panoramic views of the city skyline, the Hudson River, the New York Harbor, and the Statue of Liberty through its wraparound floor-to-ceiling windows, the previous listing notes.

The home is considered to have one of the largest outdoor spaces in Manhattan, totaling 3,821 square feet surrounded by manicured gardens.

Features of the unit include an open kitchen with signature millwork and blue de savoie stone island countertops.

All bedrooms come with ensuite bathrooms. The double-exposure primary bedroom features an expansive closet, a dressing room and a spa-like ensuite bathroom with heated floors.

Smart-home ready, the residence also features beamed ceilings and pre-war window fenestrations.

Situated in a full-service building, it has a 24-hour concierge, a live-in resident manager and a slew of amenities, which include a second-floor 1,200-square-foot fitness center with yoga and training studios, a children’s playroom, two residents’ lounges, cold storage, private and bicycle storage and a theater-quality screening room.

While the monthly price is the highest on record, sources told The Real Deal, that other units downtown have rented for more. Unlike sales, rentals are not publicly recorded in order to verify.

“It’s the highest [rent] I’m aware of,” Jonathan Miller, whose appraisal firm Miller Samuel prepares market reports for Douglas Elliman, told the outlet.

From NY Post:

Five people were injured, including a firefighter, when a crane collapsed into a neighboring building after catching fire in New York City on Wednesday morning, authorities said.

The construction equipment and debris fell near 41st and 10th Avenue in Manhattan around 7:40 a.m, the FDNY said.

The five injured people suffered non-life-threatening injuries.

From W42st.com

On Friday, New York started installing the first of the 120 toll readers on W61st Street and West End Avenue, which will be empowered to monitor and charge congestion fees for drivers heading below 60th Street in Manhattan from Spring 2024.

When we dropped by to take photographs of the newly installed cameras, a driver was double parked in the street, shooting a video for his social media account. Jimmy Gomez, known on Instagram as @blacktiger12, posted and shared with his colleagues: “The city is ready to kill us with the tolls. Enjoy!” Gomez lives in the Bronx and is an UBER driver. He said that even though the city might charge the livery drivers just once a day, it was an extra cost they could not afford, adding: “But for the people who are coming to the city, it’s gonna be insane.”

Gomez is not the only one against the congestion charges. Phil Murphy, the Governor of New Jersey, filed a lawsuit to block New York’s congestion tolling program on Friday. Governor Murphy said on social media that he wanted to prevent the implementation of the controversial charges, suggesting that the federal government may have side-stepped conventional channels. Murphy said that the tolls were “anti-environmental, anti-commuter and anti-business.”

July 19, 2023 Ciara Long, Bisnow New York City

From Bisnow:

The owner of a nine-story office condominium in Manhattan’s Garment District has fallen behind on its debt obligation after the building’s sole office tenant stopped paying rent.

The loan backing the commercial portion of the 18-story 315 West 36th St. building, built in 1926, is now in special servicing, according to the Morningstar Credit database. The building’s owner, Walter & Samuels, has been in default since April, according to commentary by special servicer Midland Loan Services.

The largest tenant in the property WeWork, signed a lease in 2015 covering roughly 135K SF across all nine floors of office in the building. But WeWork has stopped paying rent, according to the special servicer commentary, and is not planning to renew its lease for the space.

The building has 143K SF of leaseable space, including ground-floor retail. Walter & Samuels took out a $77M loan at the building in 2018, which matures in March 2028. Walter & Samuels, led by David Berley, paid SL Green $115M for a 35.5% stake in the building a few months after WeWork signed its lease.

WeWork doesn’t list the building on its website, but does offer coworking space down the block at 229 West 36th St.

The building has nine stories of residential condos atop the commercial property and spans 276K SF in total. Ratings agency Fitch signaled in early June that the property’s CMBS debt could face a credit downgrade, Crain’s New York Business reported.

The lender and special servicer have executed a pre-negotiation letter and are starting workout discussions for the space, according to the servicer commentary.

Representatives for Walter & Samuels and WeWork declined to comment to Bisnow.

WeWork’s contraction efforts in recent years have led to upheaval in the office markets it operates in. After closing scores of locations in the early months of the pandemic, it announced last fall it would close 40 more as its losses mounted. It was sued in Chicago earlier this year for vacating a property it agreed to lease until 2033.

In one instance, WeWork stopped paying rent to itself. At 600 California St. in San Francisco, a building in which WeWork has a 3% ownership stake and occupies more than 50%, loan documents indicate it stopped paying rent earlier this year, Bisnow previously reported.

From the Gothamist

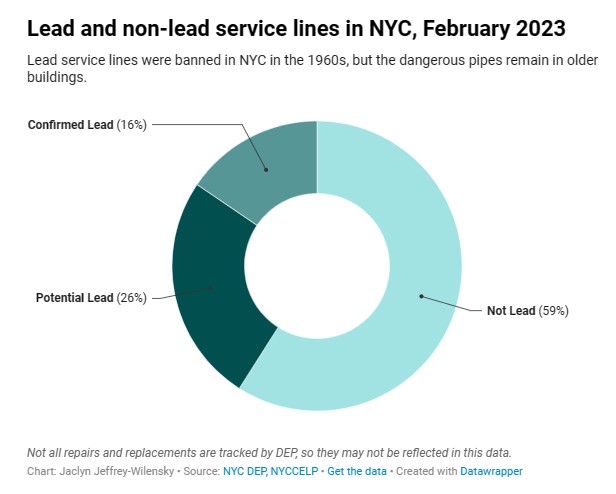

Lead pipes may carry water to as many as 900,000 New York City homes, more than 60 years after such pipes were banned across the five boroughs, according to a new report by the New York City Coalition to End Lead Poisoning.

By analyzing publicly available data from the city’s Department of Environmental Protection, the report found that nearly half of all buildings in Brooklyn and Manhattan are served by pipes that are either certainly or potentially made of lead, a dangerous heavy metal that can cause permanent brain damage and other developmental problems in children if consumed. Staten Island’s Port Richmond had the highest proportion among individual neighborhoods.

The pipes need to be replaced for the health of the public, said Joan Matthews, senior attorney with the Natural Resources Defense Council, which contributed to the report. That’s why she and the report’s other authors want the City Council to pass a bill mandating that city agencies replace the lead pipes within the next decade.

New York City treats its water to prevent corrosion, the chemical reaction by which lead flakes off the pipes and into the water supply, according to the Department of Environmental Protection. “While we agree that privately-owned lead service lines should be removed, and are actively working to do that, NYC’s daily water supply is safe,” DEP Commissioner Rohit Aggarwala said via an emailed statement.

But lead levels can still spike depending on the temperature of the water and the time since it was last turned on. Nearly a decade ago, Flint, Michigan experienced a lead crisis after merely switching what water source went through its pipes.

New York City outlawed new installations of lead service lines — the pipes that carry water from central mains to individual buildings — in 1961. But many of the predating lead service lines are still underground, and because so much time has passed, it’s unclear exactly how many remain.

For the new report, the data team for the NYC Coalition to End Lead Poisoning — a group of experts and advocates that’s been campaigning for the cause since the 1980s — studied lead service line records published biannually by the Department of Environmental Protection. The city agency identifies confirmed lead service lines throughout the five boroughs. It also labels a pipe “potential lead” if historical records indicate that at least a portion of the water service line is lead. But it’s hard to know for sure because the pipes were installed so long ago.

The report’s authors classified the number of each service line by neighborhood and joined the counts with population data to estimate how many New Yorkers use the poisonous pipes.

The report found about 40% of citywide service lines include some lead pipe. Those service lines provide water to an estimated 1.8 million people, or more than 20% of the city’s population.

Brooklyn and Manhattan led the city in the estimated proportion of lead service lines, at 46% and 44%, respectively. The Bronx, meanwhile, had the largest chunk of confirmed lead service lines of all the boroughs.

Staten Island had a below-average proportion of lead service lines at the borough level, but its Port Richmond neighborhood, situated on its North Shore, had the largest share by far of lead service lines: an estimated 61% of its pipes are either believed or confirmed to contain lead. East Harlem, Coney Island in Brooklyn and Jamaica in Queens also ranked high on the list of neighborhoods most plagued by lead service lines.

BY: MICHAEL YOUNG AND MATT PRUZNICK

From Yimby

Construction is complete on The Parluxe, an eight-story mixed-use building at 71-82 Parsons Boulevard in Kew Gardens Hills, Queens. Designed by ARC Architecture and developed by A&R Properties Group, the all-electric structure spans 100,000 square feet and yields 94 rental units in studio to two-bedroom layouts with interiors by Durukan Design, as well as 8,000 square feet of community facility space and 45 enclosed parking spaces. REAL New York is handling marketing and leasing for the property, which is bound by Parsons Boulevard to the east, Aguilar Avenue to the west, and 72nd Avenue to the south.

Recent photos show the completed look of the façade, which is composed of light gray bricks, ACM metal and wooden paneling, and floor-to-ceiling windows and sliding doors. There are multiple stacks of balconies lined with glass railings, and an expansive roof terrace surrounds the upper volume of the building. The ground-floor community facility can be subdivided into three spaces measuring 1,900 square feet, 3,850 square feet, and 2,250 square feet, or be activated by a single tenant.

From NYTimes.com

July 12, 2023

Inflation cooled significantly in June, offering some of the most hopeful news since the Federal Reserve began trying to tame rapid price increases 16 months ago — and boosting the chances that the central bank might be able to stop raising interest rates after its meeting this month.

The Consumer Price Index climbed 3 percent in the year through June, according to data released Wednesday, less than the 4 percent increase in the year through May and just a third of its roughly 9 percent peak last summer.

That overall measure is being pulled down by big declines in gas prices that could prove ephemeral, which is why policymakers closely watch a more slimmed-down version: the change in prices after stripping out food and fuel costs. That metric, known as the core index, offered news that was even better than what economists had expected.

The core index climbed 4.8 percent compared with the previous year, down from 5.3 percent in the year through May. Economists had forecast a 5 percent increase. And on a monthly basis, it climbed at the slowest pace since August 2021.

Slower inflation is unquestionably good news, because it allows consumer paychecks to stretch further at the gas pump and in the grocery aisle. And if inflation can come down sustainably without a big increase in unemployment or a painful economic recession, it could allow workers to hang on to the major gains they have made over the past three years: progress toward better jobs and pay that has helped to chip away at income inequality.

The White House, which has spent over a year on the defensive over rising prices, celebrated the fresh report, with President Biden calling the current economic moment “Bidenomics in action.” And stocks soared as investors bet that the Fed would be able to be less aggressive in its fight against inflation — even halting its interest rate increases after a final July move — in light of the new data.

“This is very promising news,” said Laura Rosner-Warburton, senior economist and founding partner at MacroPolicy Perspectives. “The pieces of the puzzle are starting to come together. But it’s just one report, and the Fed has been burned by inflation before.”

Fed officials are likely to avoid declaring victory just yet. Policymakers are still trying to assess whether the moderation is likely to be quick and complete. They do not want to allow price increases to linger at slightly elevated levels for too long, because if they do, consumers and businesses could adjust their behavior in ways that make more rapid inflation a permanent feature of the economy.

That’s why officials have signaled in recent weeks that they are likely to raise interest rates at their meeting on July 25 and 26. Policymakers had also indicated that one or more additional rate moves could be warranted after that.

Manhattan Real Estate tracker has learned that the building that currently houses Gristides Supermarket and other stores will be torn down for a new residential development that will be anchored with a large 27,000 square foot Lidl Supermarket. The property will be developed by MAG Partners.

From MAG Partners:

MAG Partners was selected by Penn South, the affordable housing cooperative in Chelsea, to develop 335 Eighth Avenue into a mixed income apartment building with ground floor commercial space, including a grocery store. The new 190-unit building will be developed under the Affordable NY Program with thirty percent of its units reserved for low- and middle-income New Yorkers.

The redevelopment will replace the aging existing building with a modern, contextual seven-story building that is about 200,000 square feet, designed by renowned local architects COOKFOX. At the heart of Penn South, the design seeks to bridge the historical character of Chelsea, 21st century visions of urban living and contemporary aspirations for a new building that supports sustainable and healthy living.