Real Estate Agents Rally to Stop Intro 360 at New York City Hall

By Manhattan Real Estate Tracker, June 12, 2024

Real estate agents and brokers came out this morning to City Hall in Downtown Manhattan today to rally against Intro 360 which would require only those who hire a real estate agent to the broker fee. While all commissions are negotiable, typically the broker fee for leasing an apartment is 15 percent of the first year’s rent. New York City is unlike any city in the country, Manhattan Real Estate Tracker strongly opposes Intro 360.

According to the co-sponsor of the measure, City Council member Chi Ossé, renters deposit $10,000 on average for a new home. One major expense he wants to eliminate is the mandatory broker fee. However, landlords will simply raise the rent and in the long run, the renter would have paid more in rent than if they paid a broker fee and received a lower starting rent.

Tenants claim that they had to pay the broker fee even though “they didn’t hire a broker.” When an agent markets an apartment for rent and a potential tenant inquires about it, it was the agent’s experience and knowledge of real estate and marketing that not only secured the exclusive listing but also generated the call. This work has value and in certain cases, the agent should be compensated by the renter.

Links to local online articles regarding today’s rally and Intro 360 from local New York television stations can be found below.

Manhattan Real Estate Tracker will be attending the rally at City Hall on Wednesday, June 12, 2024 to oppose Int. 360. This bill would stop real estate brokers and agents of a landlord from collecting a broker’s fee from a renter. All agents and brokers can attend to support the opposition of this bill.

The City Council states, “This bill would require an individual who is a representative or an agent of a property owner or a prospective tenant in a residential rental real estate transaction to collect fees charged in the transaction from the party employing the individual. The provisions of this bill would not impact the collection of fees by a landlord or property owner.”

One of the first buildings protected by New York City as a landmark could be in danger of being destroyed. The team at the Merchant’s House said they believe construction that has been approved next door could cause irreversible damage.

Take away the modern plumbing and electrical upgrades, Merchant’s House is a 19th century single-family home preserved inside and out, according to Pi Gardiner, the museum’s executive director.

What You Need To Know

Merchant’s House is a 19th century home that has been preserved inside and outside

It is a landmark at the local, state and federal level

Engineers and attorneys representing the home believe construction next door could damage, even destroy, the landmark

The Landmarks Preservation Commission said they believe a stricter standard of precautions were approved for the project to move forward

“This is one of a kind,” she said. “There’s nothing like it.”

Nearly 60 years ago, the Landmarks Preservation Commission was empowered to protect historic sites around the five boroughs. Gardiner said Merchant’s House was the first approved by the commission in Manhattan.

Yet now, she and others are afraid it could be in danger.

“This is the most dangerous project I’ve seen approved in the 30 years I’ve been doing this work,” said Michael Hiller, a lawyer who is representing Merchant’s House.

He has been fighting against the proposed development of a garage next door.

In 2018, NY1 covered the effort by a developer to build a hotel. It was a project the LPC approved in 2014. Hiller had concern about the construction next door damaging Merchant’s House.

Ultimately, the City Council rejected it.

However, this past December, the LPC approved a new project to turn that garage into a commercial office building.

An LPC spokeswoman said the passage came with contingencies to protect Merchant’s House. There were 10 listed, including more testing for soil conditions, requiring excavation of the building to be further from Merchant’s House and enhanced vibration monitoring from construction.

It also requires real-time notification to Merchant’s House of construction updates and data.

The spokeswoman called it “stricter than what is normally required under current building code.”

Hiller said, though, he’s not convinced and doesn’t even believe the LPC reviewed the documents Merchant’s House engineers submitted. He pointed out the following exchange in the December meeting.

“Has the Merchant’s House reviewed this plan? And have they any comments on it,” said one of the commissioners to the developer’s engineer.

“Yes. Yes they have,” responded the engineer.

“Do they have a consulting engineer or somebody who is advising them on this,” asked that same commissioner.

The commissioner was seemingly unaware Merchant’s House in fact has a consulting engineer, who submitted a report to the commission chair four days before the meeting. The report claims the developers’ engineers may have incorrectly calculated the weight of the building and that foundation shifting could be three times the allowable limit.

While the developer’s engineers pledged to stop construction at a threshold below the foundational shifting limit, Hiller did not believe the project would truly stop. He said, furthermore, the problem is that no one seemed aware of the potential issue.

“The fact is none of them spoke up because none of them had read the materials,” said Hiller.

Hiller said he was further convinced when the commission asked for a new study on the potential impact construction could have on Merchant’s House’s plaster, which is from the 19th century.

Hiller said engineers for Merchant’s House did a plaster study 10 years ago, raising questions and concerns about the impact from next door construction.

While the commissioners said they received more than 600 emails in opposition to the project, it was approved in December.

“Keeping our city’s landmark buildings safe and secure is a top priority, and when considering proposals for work adjacent to designated properties, the agency coordinates closely with DOB and requires building owners to use enhanced safeguards to protect these landmark buildings when appropriate,” said an LPC spokeswoman in an emailed statement to NY1. “Regarding Merchant’s House Museum, the Commission required that proposed work on the adjacent property at 27 E. 4th Street include stringent measures to ensure the integrity of Merchant’s House. The plan approved by the Commission includes stabilization and protective methods that are stricter than what is normally required under current building code, and includes enhanced monitoring and real-time notifications.”

In a city always changing and growing, Merchant’s House has stood the test of time. Its leadership said the question now is whether it will continue to.

Advance Estimates of U.S. Retail and Food Services

Advance estimates of U.S. retail and food services sales for April 2024, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $705.2 billion, virtually unchanged (±0.4 percent) from the previous month, but up 3.0 percent (±0.5 percent) above April 2023. Total sales for the February 2024 through April 2024 period were up 3.0 percent (±0.5 percent) from the same period a year ago. The February 2024 to March 2024 percent change was revised from up 0.7 percent (±0.5 percent) to up 0.6 percent (±0.1 percent).

Retail trade sales were virtually unchanged (±0.4 percent) from March 2024, but up 2.7 percent (±0.5 percent) above last year. Non-store retailers were up 7.5 percent (±1.6 percent) from last year, while food services and drinking places were up 5.5 percent (±2.1 percent) from April 2023.

Permits have been filed for an 11-story mixed-use building at 489 Ninth Avenue in Manhattan’s Midtown West. Located between West 37th and West 38th Streets, the lot is four blocks from 34th Street-Penn Station subway station, serviced by the A, C, and E trains. Susan Wu of ZD Jasper Realty is listed as the owner behind the applications.

The proposed 120-foot-tall development will yield 63,264 square feet, with 57,250 square feet designated for residential space and 6,013 square feet for commercial space. The building will have 59 residences, most likely condos based on the average unit scope of 970 square feet. The concrete-based structure will also have a cellar and a 30-foot-long rear yard.

Governor Kathy Hochul today announced a $2.2 million expansion of New York’s Fair Housing Testing Program designed to root out discrimination in home rental and sale transactions. New York State partnered with six nonprofit organizations across the state to deploy undercover testers to act as potential renters and home seekers. The expansion will increase proactive investigations of suspected housing discrimination and enhance education and outreach efforts on fair housing rights, including for individuals with a history of criminal system involvement.

“As we expand access to housing across New York State, I am using all of the resources at my disposal to combat housing discrimination and ensure that all New Yorkers are treated with dignity, fairness, and respect when seeking the housing of their choice,” Governor Hochul said. “Our investment in this crucial program sends a clear message: housing discrimination will not be tolerated here in New York.”

The Fair Housing Testing Program is administered by New York State Homes and Community Renewal’s Fair and Equitable Housing Office and expands the pilot testing program established by the office in 2021. The program also provides continuity to the Eliminating Barriers to Housing New York testing and outreach program launched by the New York Office of the Attorney General in partnership with Enterprise Community Partners.

HCR has finalized contracts with six organizations to conduct testing in 48 counties including Nassau and Suffolk, Westchester, Albany and Schenectady counties, as well as the five boroughs of New York City. The fair housing testing and outreach partners are: CNY Fair Housing, the Fair Housing Justice Center, Housing Opportunities Made Equal, Legal Assistance of Western New York, Long Island Housing Services, and Westchester Residential Opportunities. These nonprofit housing agencies will dispatch trained fair housing “testers” to act as potential renters or home seekers to uncover unlawful discriminatory treatment by sellers, brokers, and landlords.

The program’s outreach and training will focus on fair housing protections including for those with arrest and conviction histories. The outreach includes advertisements and social media messaging, training events, and professional education classes.

New York State Homes and Community Renewal Commissioner RuthAnne Visnauskas said, “Housing is an essential human right and we must continue to use every tool at our disposal to ensure that all New Yorkers have a fair and equal opportunity to live in the communities of their choice. Our Fair Housing Testing program complements Governor Hochul’s New York Housing Compact, which will proactively address disparities in housing access, exclusionary zoning, and other barriers that impede fair housing goals, and help us build a better and more equitable New York for all.”

More information on Fair Housing can be found on HCR’s website: hcr.ny.gov/feho.

Marlene Zarfes, Executive Director of Westchester Residential Opportunities, said, “This work is critical to ensuring a housing market in the Lower Hudson Valley in which every household has an equal opportunity to participate, regardless of skin color, ethnicity, source of income, disability or any other protected class.”

Elizabeth Grossman, Executive Director of the Fair Housing Justice Center, said, “The Fair Housing Justice Center is immensely grateful for this support from HCR and we are eager to get to work on new testing and outreach activities. Testing remains a critical tool for fair housing organizations to use in the fight against discrimination, and we look forward to conducting robust investigations throughout the New York City region. The outreach funding will provide an enhanced opportunity for us to increase awareness of fair housing rights and responsibilities, especially the strong protections that New York State has put in place to counter source-of-income discrimination, and to provide training to tenants, home seekers, and housing providers. Thanks to the support of HCR, people throughout our service area will know that they can come to us for help, and that our programs will get them the help they need.”

Ian Wilder, Executive Director of Long Island Housing Services, said, “Long Island Housing Services is grateful to New York State for supporting much needed fair housing work. This funding allows us to assist in enforcing the very necessary protections afforded under New York State law. Even more so, it enables Long Islanders move toward a home that we all strive for where our neighbors can choose to live wherever they want free of discrimination. Only by overcoming housing discrimination can we free Long Islanders to live their best lives.”

DeAnna Eason, Executive Director of Housing Opportunities Made Equal, said, “Education and outreach are imperative to the eradication of discrimination in housing and the furtherance of fair housing. HOME appreciates the support of NYSHCR in combating bias in housing, and the promotion of diversity and equality in our communities.”

Sally Santangelo, Executive Director of CNY Fair Housing, said, “CNY Fair Housing has a long history of fighting barriers to housing in the Syracuse region. With this funding, we will be able to conduct more fair housing testing and outreach to our region and beyond. We look forward to continuing partnership with New York State Homes and Community Renewal to eliminate discrimination in housing.”

Programs for regulating rent, known as rent control and rent stabilization, are in place in several communities around New York State. Rent regulation has two purposes: first, to shield tenants in privately held buildings from unlawful rent hikes; second, to enable building owners to maintain their properties while making a fair profit. Of the two rent regulation schemes, rent control is the more established one. It was first implemented in response to the housing scarcity that followed World War II and is typically applicable to structures built before 1947. In general, rent stabilization applies to apartments that were freed from rent control and buildings constructed after 1947 but before 1974. It also includes buildings that are eligible for tax incentives under J-51, 421-a, and 421-g. The apartments that are eligible for these tax benefit programs are determined by their own set of regulations.

Rent stabilization outside of New York City is also referred to as ETPA, or the Emergency Tenant Protection Act, and it’s legal in a few counties and places (see Fact Sheet #8). Rent stabilization can also apply to housing accommodations whose rentals are set by public benefit corporations, DHCR, and other government bodies, as outlined in the rent regulations.

Rent Stabilization In addition to limiting the amount of rent increases, rent stabilization offers tenants protections. Tenants are entitled to the provision of necessary services, the renewal of their leases, and are not subject to eviction unless there are legally permissible reasons. Tenants have the option to extend their leases for one or two more years. Tenants can use a number of forms developed by the Division of Housing and Community Renewal (DHCR) to make pertinent complaints. After serving the owner with the complaint and gathering evidence, DHCR must issue a formal order that is appealable.

DHCR has the authority to lower rent and impose civil penalties on the owner in cases when a tenant’s rights are infringed. Should you fail to maintain services, your rent may be lowered. If there is an overcharge, the DHCR may impose interest penalties or triple damages that must be paid by the tenant.

Rent Control Rent control restricts the amount of rent an apartment owner can charge as well as the owner’s ability to evict residents. Additionally, tenants are entitled to certain necessities. Since tenants are regarded as “statutory” tenants, owners are not obligated to provide renewal leases. Tenants can use a number of forms developed by DHCR to file pertinent concerns. After serving the owner with the complaint and gathering proof, DHCR is authorized to issue a written order that is appealable. Rents may be lowered and civil penalties may be imposed by DHCR on the owner in the event that a tenant’s rights are infringed. Reduced rent is a possibility if services are not kept up. When there is an overcharge, the DHCR may determine the legally collectible rent.

Please refer to an attorney for legal advice regarding your specific situation. Additional information can be found at the Department of Homes and Community Renewal.

Elected officials, scientists, bird experts and New Yorkers held a City Hall rally Thursday to announce the introduction of the historic package of bills.

Flaco died after eating pigeons infected with virus and was exposed to rat poison before flying into an Upper West Side building on Feb. 23.

Council Member Shaun Abreu introduced the first of three pieces of “Flaco’s Laws” to stem unnecessary bird deaths like Flaco’s. One part of the bill would require the health department to replace rat poison with rat birth control.

“Flaco’s autopsy confirmed our worst fears: he ingested a fatal dose of rat poison. Rodenticides are not only toxic for the animals we love, they are increasingly ineffective at reducing rat infestations. It’s time we put new practices in place to build a better, safer, more eco-friendly city,” said Abreu said. “We can’t poison our way out of the rat problem, but we can certainly do a lot of damage trying.”

Another bill would address light pollution and reflective windows on buildings that disorient birds.

Flaco was freed from his cage at the Central Park Zoo in early 2023 by a vandal who breached a waist-high fence and cut a hole through a steel mesh cage. The owl had arrived at the zoo as a fledgling 13 years earlier.

Zoo officials and his fans were at first worried about his survival, but he soon proved adept at catching rats and other prey. The zoo later suspended efforts to re-capture him after failed attempts.

Flaco’s death was a heartbreaking end for the birders who documented his daily movements and the legions of admirers who followed along, as people posted photos and videos of the majestic owl with a nearly 6-foot wingspan perched on tree branches, fence posts, fire escapes and water towers – as well as his hours of hooting.

In addition to the package of bills introduced Thursday, a tattoo parlor in Brooklyn offered discounted tattoos of the beloved bird from noon to 7 p.m. They were offered at East River Tattoo in Greenpoint and cost $150 with tips donated to the Wild Bird Fund.

“It’s something that people connect to on a personal level and just their own struggle to exist in a challenging place to live,” said tattoo artist Duke Riley.

The package of bills will eventually go through the Sanitation Committee before going to a committee and then will be voted on.

Efforts are also underway to put a statue of Flaco in Central Park.

(The Associated Press contributed to this report.)

For all of modern American history, the movie theater has been a cornerstone of our culture.

It has become a gathering point for families, friends and maybe a first date.

And for more than 30 years, people in the Bronx turned to Concourse Plaza Multiplex Cinemas, but next month, the theater that has housed laughs, cries and everything in between, will shut its doors.

The theater first opened its doors in 1991 when “Home Alone” and “Thelma & Louise” were screening, but just ahead of summer, the final film will flicker across the theater’s iconic screens.

Locals are convinced the boom in digital platforms has made the movie-going experience more irrelevant.

“All these streaming networks, that’s probably what it is. Instead of spending money on movies, they probably just want to stay home,” resident Brook Schuler said.

The Bronx has just two theaters left. Once the multiplex shuts down, moviegoers will have to make their way to Bay Plaza in Co-op City.

Showcase Cinemas, the parent company of Concourse Plaza Multiplex Cinemas, was apparently unable to reach a new lease agreement.

Bronx Borough President Vanessa Gibson says the shutdown does not come as much of a shock.

“This is happening across the board where you sometimes have landlords and owners that are raising the price exorbitantly where the tenants can no longer afford it and they’ll say it’s not worth it anymore,” Gibson said. “We’re losing customers, we’re losing revenue, we can’t meet payroll and we just can’t maintain a business we’re operating at a deficit and no one wants to do that.”

Meanwhile, Feil, the landlord of Concourse Plaza, rejects claims that a new leasing deal could not be reached.

“Despite negotiating with the theater company and getting them to renew the lease, they chose to leave the community,” a representative for the company said

They said they are hoping to replace them with another theater.

The theater is just the latest entity in the once bustling shopping center on 161st Street to shutter. A food court and a grocery store also closed their doors for good in recent years.

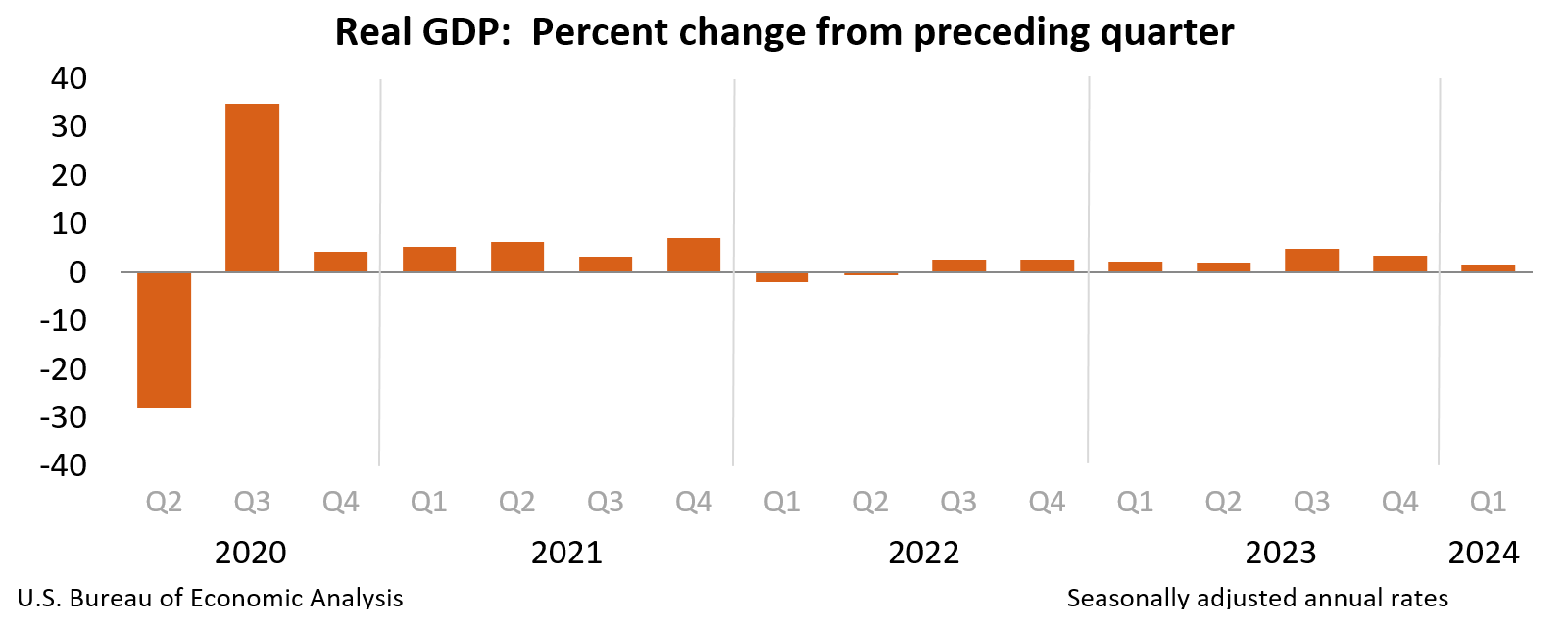

From the US Department of Commerce Bureau of Economic Analysis.

Real gross domestic product (GDP) increased at an annual rate of 1.6 percent in the first quarter of 2024 (table 1), according to the “advance” estimate released by the Bureau of Economic Analysis. In the fourth quarter of 2023, real GDP increased 3.4 percent.

The GDP estimate released today is based on source data that are incomplete or subject to further revision by the source agency (refer to “Source Data for the Advance Estimate” on page 3). The “second” estimate for the first quarter, based on more complete source data, will be released on May 30, 2024.

The increase in real GDP primarily reflected increases in consumer spending, residential fixed investment, nonresidential fixed investment, and state and local government spending that were partly offset by a decrease in private inventory investment. Imports, which are a subtraction in the calculation of GDP, increased (table 2).

The increase in consumer spending reflected an increase in services that was partly offset by a decrease in goods. Within services, the increase primarily reflected increases in health care as well as financial services and insurance. Within goods, the decrease primarily reflected decreases in motor vehicles and parts as well as gasoline and other energy goods. Within residential fixed investment, the increase was led by brokers’ commissions and other ownership transfer costs as well as new single-family housing construction. The increase in nonresidential fixed investment mainly reflected an increase in intellectual property products. The increase in state and local government spending reflected an increase in compensation of state and local government employees. The decrease in inventory investment primarily reflected decreases in wholesale trade and manufacturing. Within imports, the increase reflected increases in both goods and services.

Compared to the fourth quarter, the deceleration in real GDP in the first quarter primarily reflected decelerations in consumer spending, exports, and state and local government spending and a downturn in federal government spending. These movements were partly offset by an acceleration in residential fixed investment. Imports accelerated.

Current‑dollar GDP increased 4.8 percent at an annual rate, or $327.5 billion, in the first quarter to a level of $28.28 trillion. In the fourth quarter, GDP increased 5.1 percent, or $346.9 billion (tables 1 and 3).

The price index for gross domestic purchases increased 3.1 percent in the first quarter, compared with an increase of 1.9 percent in the fourth quarter (table 4). The personal consumption expenditures (PCE) price index increased 3.4 percent, compared with an increase of 1.8 percent. Excluding food and energy prices, the PCE price index increased 3.7 percent, compared with an increase of 2.0 percent.

Personal Income

Current-dollar personal income increased $407.1 billion in the first quarter, compared with an increase of $230.2 billion in the fourth quarter. The increase primarily reflected increases in compensation and personal current transfer receipts (table 8).

Disposable personal income increased $226.2 billion, or 4.5 percent, in the first quarter, compared with an increase of $190.4 billion, or 3.8 percent, in the fourth quarter. Increases in compensation and personal current transfer receipts were partly offset by an increase in personal current taxes, which are a subtraction in the calculation of DPI. Real disposable personal income increased 1.1 percent, compared with an increase of 2.0 percent.

Personal saving was $755.7 billion in the first quarter, compared with $815.5 billion in the fourth quarter. The personal saving rate—personal saving as a percentage of disposable personal income—was 3.6 percent in the first quarter, compared with 4.0 percent in the fourth quarter.

Source Data for the Advance Estimate

The GDP estimate released today is based on source data that are incomplete or subject to further revision by the source agency. Information on the source data and key assumptions used in the advance estimate is provided in a Technical Note and a detailed “Key Source Data and Assumptions” file posted with the release. The second estimate for the first quarter, based on more complete data, will be released on May 30, 2024. For information on updates to GDP, refer to the “Additional Information” section that follows.

* * *

Next release, May 30, 2024, at 8:30 a.m. EDT Gross Domestic Product (Second Estimate) Corporate Profits (Preliminary Estimate) First Quarter 2024