Brooklyn’s tallest building is struggling to pay its skyscraping loans.

Michael Stern, the developer of 9 DeKalb Avenue’s 93-story The Brooklyn Tower, has defaulted on a $240 million mezzanine loan and now faces foreclosure, the Real Deal has reported.

A UCC foreclosure auction has been scheduled for Jun. 10 by Silverstein Capital Partners, which issued the loan in 2019, according to marketing materials from real estate company JLL.

The Brooklyn Tower, a 93-story structure located at 9 DeKalb Avenue, is the tallest building in the borough.

“9 DeKalb’s junior mezzanine, senior mezzanine and mortgage loans are in maturity default, and the junior mezzanine lender is enforcing its junior mezzanine loan remedies through a Uniform Commercial Code (UCC) sale process,” a Silverstein spokesperson confirmed to The Post.

“The junior mezzanine lender has engaged JLL to market the equity interests securing the junior mezzanine loan, and they will conduct a public auction after a marketing period.”

Stern’s JDS Development Group did not immediately return The Post’s request for comment.

It’s unclear what will become of the tower, which only opened to tenants last year.

The news comes just days after a 440-square-foot studio in the skyscraper sold for $905,000, making it the most expensive studio in borough history, 6sqft reported.

A video producer who lives across the street previously told The Post that the building looks like “the headquarters of an evil corporation in a superhero movie.”

The apartment, unit 72A, is more than 720 feet from the street below and features floor-to-ceiling windows, and in-unit Miele washer-dryer and European white oak flooring.

“This is an incredible milestone for Downtown Brooklyn. Our newest residents will be living at the highest elevations ever available in the borough,” said Stern, who attempted to sell part of the 1,000-foot-tall Downtown Brooklyn behemoth’s rental portion in early 2023.

At the time, he put its 398 rental apartments as well as the building’s amenities — including a pool, 50,000 square feet of retail and 77,000 square feet of workout facilities provided by the upscale chain LifeTime Fitness — on the market for an ambitious $500 million.

It’s unclear what will become of the tower, which only opened to tenants last year.

But a deal was never struck for the listing, which notably did not include the 93-story skyscraper’s 143 individual residential condominiums, and now the building’s fate is up in the air.

In addition to now having a reputation for financial trouble, the looming metallic supertall has also become known for its “evil vibes.”

A video producer who lives across the street previously told The Post that the building looks like “the headquarters of an evil corporation in a superhero movie.”

Sam Ash’s Midtown store is closing for good. Photo by Dean Moses

Sam Ash’s Midtown location is reportedly closing its doors for good. It was reported by w42st.com that the famed store, located at 333 W 34th St., would be closing down after a century of business in the neighborhood. Originally founded in 1924, the music chain originated in New York, with the first store opened by the Ash family in Brooklyn.

Photo by Dean Moses

The W 34th Street store is reportedly one of 18 stores that are closing across the country, which also reportedly includes Sam Ash’s Huntington Station location on Long Island and its Forest Hills location in Queens.

Liquidation signs appeared in the windows of the Midtown store, signaling sales and the store’s impending closure.

“For the last 100 years, Sam Ash Music has successfully adapted to meet the challenge of changing business conditions. As we look towards the next 100 years, the company must continue to adapt to ensure its continued success,” Sam Ash told amNewYork Metro in a statement. “Sam Ash Music remains committed to keeping a strong physical store footprint in the future while we continue growing our successful online sales offerings. As part of this restructuring, the company is closing several stores nationwide. This restructuring is emotionally tough, but we are confident these moves will make Sam Ash Music stronger as we continue serving the music community into the future, as we have for the past 100 years.”

Manhattan Real Estate Tracker visited the store yesterday and most items are now 10% with no returns accepted.

Manhattan Real Estate Tracker has learned that Avi Hiaeve, the founder and CEO of the luxury timepiece and jewelry firm Avi & Co., purchased the former Playboy Club building at 5 East 59th Street at a foreclosure auction. The bid was approximately $26.7 million. The previous investors had purchased the property for $85 million.

The Chrysler Building is attempting to reposition itself by marketing to high-end retail tenants.

The iconic Chrysler Building has signed its first tenant following a retail makeover that aims to bring an air of modern luxury into the challenged art deco landmark.

WatchHouse, a British coffee shop that recently opened its first U.S. store at 660 Fifth Ave., will open its second location at the base of the Chrysler Building. It signed a lease for 2K SF on 43rd Street, across from an entrance to Grand Central Terminal.

Retail by Mona CEO Brandon Singer, who led broker teams that represented the tenant and landlord RFR, said the lease reflects the vision for the building’s retail.

“It’s creating a destination for retail that is a little bit outside of the box, given the amazing asset,” Singer told Bisnow. “With all the dense office buildings in this area, this will help the people coming back to work. Give them an experience that they may not have had in the past.”

As tenants opt for amenity-rich, Class-A towers, owners of historic buildings like the Chrysler Building are attempting to find a role for their properties to play in a remote work world.

Singer’s team is marketing several spaces on the 1,046-foot-tower’s ground floor, in addition to storefronts on the arcade level, which totals 30K SF alone. RFR is also considering adding retail use to the second floor.

It is reinventing the Cloud Club lounge on the 61st and 62nd floors as part of a renovation that RFR co-founder Aby Rosen told Bloomberg in 2020 would cost at least $200M.

“We wanted to create something nice — food, wine, dry cleaning, shavers, hairdressers — so tenants have a reason to stay longer instead of running out,” Rosen told Bloomberg at the time.

Singer declined to provide further details on the building’s upgrades. RFR declined to comment.

The Chrysler Building previously housed retail tenants that served daily Midtown commuters, including a barbershop, a shoeshine, a dry cleaner, a locksmith and an optometrist — but all of them vacated in 2020. In its next chapter, the building will focus on higher-end tenants that could appeal to shoppers outside of the 9-to-5 work schedule, Singer said.

Most recently, the building, once the world’s tallest, has been caught in the collapse of Austrian property company Signa. The firm, founded by investor René Benko, filed for insolvency in November, and it is looking to unload its 50% stake in the skyscraper.

Rosen had been in talks to renegotiate the building’s long-term ground lease with The Cooper Union since he and Signa acquired the leasehold in 2019. Signa’s insolvency complicated those efforts, and RFR is on the hook for more than $31.5M in annual ground rent payments, the New York Post reported in November.

The Chrysler Building’s retail repositioning is similar to that of its rival Empire State Building. Empire State ownership added a three-story Starbucks Reserve store to its retail base in 2022. In 2019, it debuted a $165M redevelopment, which added a museum and made improvements to its observatory.

Empire State Realty Trust, the owner of the Empire State Building, said in its annual report that the observatory generated $129.4M in revenue, a sixth of the REIT’s total from last year. The 91K SF of retail in that building was 76.4% leased at the end of 2023.

NEW YORK — Five years after Albany Democrats overhauled the state’s rent-stabilization laws, real estate executives are looking to weaken the reforms — bolstered by data they commissioned that validates their case.

New findings from a survey of 781 property owners and managers covering about 242,000 units contend the 2019 changes led to disinvestment and substantial vacancies in rent-stabilized housing. A significant share of respondents said it is “economically infeasible” to invest in needed upgrades to their buildings. The study, obtained by POLITICO, was conducted by consulting firm HR&A Advisors on behalf of the Real Estate Board of New York and the Rent Stabilization Association. While the findings are unsurprising, real estate leaders are using them to fuel their argument against the 5-year-old legislative changes.

The issue is now entering the early stages of negotiations in Albany, amid broader discussions around a wide-ranging deal to tackle an acute housing shortage.

Tenant activists and progressive lawmakers are already pushing back on any attempt to reverse the reforms, which starts out as a tall order in the Democratic-led state Legislature.

“This data indicates that the 2019 rent law changes are having increasingly negative impacts on rent-stabilized apartments and tenants,” James Whelan, president of REBNY, said in a statement. “State lawmakers should follow the data and advance policies that facilitate the rehabilitation of dilapidated apartments in a manner that results in quality affordable housing without recreating the dynamics of vacancy decontrol.”

Real estate groups argue the 5-year-old changes — which eliminated or significantly curtailed avenues to raise rents on the city’s roughly 1 million rent-regulated apartments — have left landlords unable to rehab apartments and rerent them when long-term tenants move out.

The idea — called “self serving” by a leading tenant activist — has gained traction among some moderate Democrats: A bill introduced last year by state Sen. Leroy Comrie and Assemblymember Kenny Burgos would allow rent-stabilized landlords to reset rents at vacancy to facilitate renovations. The current law allows only very limited increases if an owner is making an apartment or building improvement.

Some prominent legislators see Comrie’s introduction as a non-starter and question the industry’s claims.

“They’re saying, let’s turn the rent-regulation system on its head because we have many units that are in dire disrepair — I don’t buy that,” said Assemblymember Linda Rosenthal, chair of the body’s housing committee. “Many of my colleagues oppose that vehemently, so I don’t think it will gain much traction, and it shouldn’t. This is not the time to be trying to undo tenant protections.”

The survey found that for owners with small portfolios that are primarily rent-stabilized — those under 11 units — 25 percent of their apartments are currently vacant.

There are also fewer total vacant apartments than there were in 2018, but longer-term vacancies — defined as three years or more — have increased, the REBNY-commissioned survey found. And nearly one-third of respondents cited “economic infeasibility” of unit improvements after a long tenancy as a reason for continued vacancies.

RSA supports the bill introduced by Comrie and Burgos. REBNY is not pushing that specific legislation but said it agrees with its general goals, and sees it as one potential approach.

“There’s no way to adjust rent at vacancy anymore in the rent-stabilized universe,” Basha Gerhards, senior vice president of planning at REBNY, said in reference to landlords’ reported drop in operating income. “So do we allow some form of rent reset in exchange for the apartments being improved and the violations being cleared? It’s a question we are posing.”

State lawmakers are under pressure to take action on housing issues this year as the city struggles with the lowest rental vacancy rate in 50 years and residential construction slows amidst the absence of a key multi-family housing tax break.

After Democrats took control of the chamber, they eliminated “vacancy decontrol” — a mechanism that allowed units to leave the rent-stabilization program when they reached a certain threshold and became vacant. They additionally got rid of a provision that permitted landlords to raise rents by 20 percent when apartments became vacant, and significantly restricted rent increases attached to building and apartment improvements.

Those provisions had led to the loss of tens of thousands of rent-regulated apartments before the 2019 reforms went into effect.

The survey found owners still need to make those upgrades — things like replacing boilers or kitchen appliances — but are pursuing fewer improvements since they no longer pencil out financially. For example, RSA members filed 763 individual apartment improvements in 2023, down from 3,311 in 2019. For individual apartment improvements, the maximum landlords can spend on renovations that would be eligible for a rent increase calculation is $15,000 over 15 years.

“Whether it’s big systems like rewiring or plumbing, or bringing [units] up to code, complying to lead paint regulations — that’s well over $15,000 for an apartment, so there’s just no incentive,” said Frank Ricci, an executive vice president at RSA.

The city’s Department of Housing Preservation and Development estimated last year there are only 2,500 low-cost apartments that are both in need of repairs and have been vacant for a year or more. The agency says that figure is significantly lower now, based on the latest housing and vacancy survey, though it has not yet released a specific number, according to Gothamist. Ricci argued smaller buildings are under-surveyed by the city survey.

“By and large, there are just not that many vacant rent-stabilized apartments in New York City right now,” said Cea Weaver, campaign coordinator for the Housing Justice for All coalition, pointing to HPD’s data. “It’s very politically convenient and self-serving to say, oh we’re in trouble because of the [2019 reforms.] But it’s like no, you’re in trouble because you speculated on buildings that are 100 years old and a pandemic happened and other costs changed.”

Weaver and other progressive activists said they’re nonetheless taking the push very seriously — and reject any attempts to include it in a broader housing agreement, even if that deal includes a longstanding priority known as “good cause” eviction. That measure would effectively limit rent hikes in market-rate apartments.

“For the left, we know what rollbacks have felt like — we experienced that in the bail reform fight,” said Jasmine Gripper, co-director of the Working Families Party. “We’ve been communicating to elected leaders that this is a non-starter.”

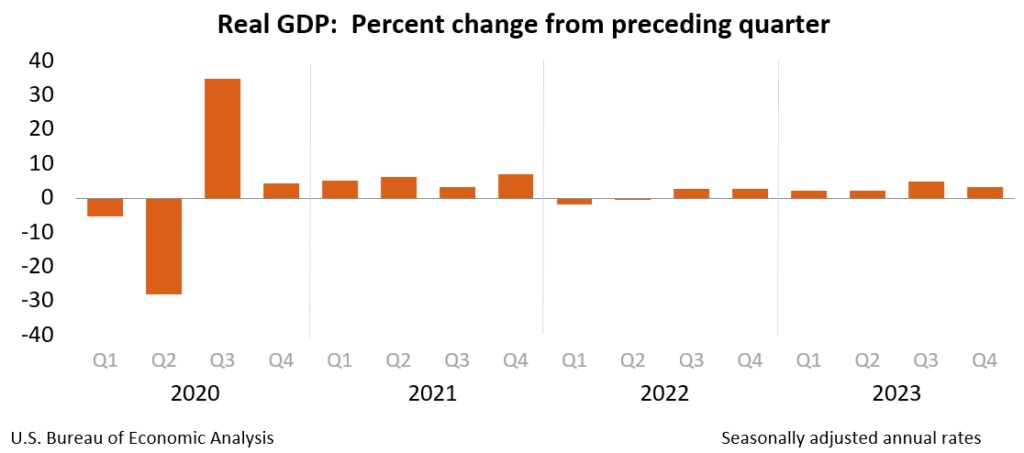

Real gross domestic product (GDP) increased at an annual rate of 3.3 percent in the fourth quarter of 2023 (table 1), according to the “advance” estimate released by the Bureau of Economic Analysis. In the third quarter, real GDP increased 4.9 percent.

The GDP estimate released today is based on source data that are incomplete or subject to further revision by the source agency (refer to “Source Data for the Advance Estimate” on page 3). The “second” estimate for the fourth quarter, based on more complete data, will be released on February 28, 2024.

The increase in real GDP reflected increases in consumer spending, exports, state and local government spending, nonresidential fixed investment, federal government spending, private inventory investment, and residential fixed investment (table 2). Imports, which are a subtraction in the calculation of GDP, increased.

The increase in consumer spending reflected increases in both services and goods. Within services, the leading contributors were food services and accommodations as well as health care. Within goods, the leading contributors to the increase were other nondurable goods (led by pharmaceutical products) and recreational goods and vehicles (led by computer software). Within exports, both goods (led by petroleum) and services (led by financial services) increased. The increase in state and local government spending primarily reflected increases in compensation of state and local government employees and investment in structures. The increase in nonresidential fixed investment reflected increases in intellectual property products, structures, and equipment. Within federal government spending, the increase was led by nondefense spending. The increase in inventory investment was led by wholesale trade industries. Within residential fixed investment, the increase reflected an increase in new residential structures that was partly offset by a decrease in brokers’ commissions. Within imports, the increase primarily reflected an increase in services (led by travel).

Compared to the third quarter of 2023, the deceleration in real GDP in the fourth quarter primarily reflected slowdowns in private inventory investment, federal government spending, residential fixed investment, and consumer spending. Imports decelerated.

Current‑dollar GDP increased 4.8 percent at an annual rate, or $328.7 billion, in the fourth quarter to a level of $27.94 trillion. In the third quarter, GDP increased 8.3 percent, or $547.1 billion (tables 1 and 3).

The price index for gross domestic purchases increased 1.9 percent in the fourth quarter, compared with an increase of 2.9 percent in the third quarter (table 4). The personal consumption expenditures (PCE) price index increased 1.7 percent, compared with an increase of 2.6 percent. Excluding food and energy prices, the PCE price index increased 2.0 percent, the same change as the third quarter.

Personal Income

Current-dollar personal income increased $224.8 billion in the fourth quarter, compared with an increase of $196.2 billion in the third quarter. The increase primarily reflected increases in compensation, personal income receipts on assets, and proprietors’ income that were partly offset by a decrease in personal current transfer receipts (table 8).

Disposable personal income increased $211.7 billion, or 4.2 percent, in the fourth quarter, compared with an increase of $143.5 billion, or 2.9 percent, in the third quarter. Real disposable personal income increased 2.5 percent, compared with an increase of 0.3 percent.

Personal saving was $818.9 billion in the fourth quarter, compared with $851.2 billion in the third quarter. The personal saving rate—personal saving as a percentage of disposable personal income—was 4.0 percent in the fourth quarter, compared with 4.2 percent in the third quarter.

GDP for 2023

Real GDP increased 2.5 percent in 2023 (from the 2022 annual level to the 2023 annual level), compared with an increase of 1.9 percent in 2022 (table 1). The increase in real GDP in 2023 primarily reflected increases in consumer spending, nonresidential fixed investment, state and local government spending, exports, and federal government spending that were partly offset by decreases in residential fixed investment and inventory investment. Imports decreased (table 2).

The increase in consumer spending reflected increases in services (led by health care) and goods (led by recreational goods and vehicles). The increase in nonresidential fixed investment reflected increases in structures and intellectual property products. The increase in state and local government spending reflected increases in gross investment in structures and in compensation of state and local government employees. The increase in exports reflected increases in both goods and services. The increase in federal government spending reflected increases in both nondefense and defense spending.

The decrease in residential fixed investment mainly reflected a decrease in new single-family construction as well as brokers’ commissions. The decrease in private inventory investment primarily reflected a decrease in wholesale trade industries. Within imports, the decrease primarily reflected a decrease in goods.

Current-dollar GDP increased 6.3 percent, or $1.61 trillion, in 2023 to a level of $27.36 trillion, compared with an increase of 9.1 percent, or $2.15 trillion, in 2022 (tables 1 and 3).

The price index for gross domestic purchases increased 3.4 percent in 2023, compared with an increase of 6.8 percent in 2022 (table 4). The PCE price index increased 3.7 percent, compared with an increase of 6.5 percent. Excluding food and energy prices, the PCE price index increased 4.1 percent, compared with an increase of 5.2 percent.

Measured from the fourth quarter of 2022 to the fourth quarter of 2023, real GDP increased 3.1 percent during the period (table 6), compared with an increase of 0.7 percent from the fourth quarter of 2021 to the fourth quarter of 2022.

The price index for gross domestic purchases, as measured from the fourth quarter of 2022 to the fourth quarter of 2023, increased 2.4 percent, compared with an increase of 6.2 percent from the fourth quarter of 2021 to the fourth quarter of 2022. The PCE price index increased 2.7 percent, compared with an increase of 5.9 percent. Excluding food and energy, the PCE price index increased 3.2 percent, compared with 5.1 percent.

Source Data for the Advance Estimate

The GDP estimate released today is based on source data that are incomplete or subject to further revision by the source agency. Information on the source data and key assumptions used in the advance estimate is provided in a Technical Note and a detailed “Key Source Data and Assumptions” file posted with the release. The “second” estimate for the fourth quarter, based on more complete data, will be released on February 28, 2024. For information on updates to GDP, refer to the “Additional Information” section that follows.

* * *

Next release, February 28, 2024, at 8:30 a.m. EST Gross Domestic Product (Second Estimate)

Mayor Eric Adams is set to use his State of the City address Wednesday to unveil a new push to use a slew of city-owned properties for affordable housing projects, The Post has learned.

The new plan will make use of public sites across the Big Apple in a bid to advance a total of 24 housing projects by the end of the year, according to an early snippet of Hizzoner’s speech obtained by The Post.

The ambitious project — dubbed “24 in 24” — will create or preserve more than 12,000 affordable homes scattered across the five boroughs, according to the mayor’s office.

“Our ’24 in 24’ plan to create and preserve affordable housing on 24 publicly-owned sites is another example of how we’re doing everything within our control to deliver housing and relief to New Yorkers when they need it most,” Adams said in a statement to The Post.

“Investments like these, once again, deliver on the vision we laid out to protect public safety, rebuild our economy, and make this city more livable for working-class New Yorkers.”

The specific plans for each property weren’t immediately available, though the Adams administration said further details on the projects and sites would be released in the coming months.

Among the locations already tipped to be part of the project is the Grand Concourse Library on 173rd Street in the Bronx and a Staten Island site located on the corner of Canal and Front streets.

The new plan will make use of public sites across the Big Apple in a bid to advance a total of 24 housing projects by the end of the year. Google Maps

At least three of the sites slated to be announced in Adams’ initial plan later Wednesday have already been floated as affordable housing developments, including 388 Hudson St. in the Greenwich Village.

In September, the city’s Department of Housing Preservation and Development had unveiled four potential renderings of the soaring building, which could rise up to 355 feet at the city-owned lot — angering some residents in the quaint neighborhood.

Two other lots in Queens — including the Hunters Point South Parcel E and a parking lot on Ninth Avenue in Inwood — are also HPD-led projects that are among the initial sites included in the mayor’s new plan.

The ambitious project — dubbed “24 in 24” — will create or preserve more than 12,000 affordable homes scattered across the five boroughs, according to the mayor’s office. nyc.gov. “While we advocate for action in Albany this session and advance our historic ‘City of Yes’ proposal, our administration is tackling the housing and affordability crisis with urgency,” the mayor said his statement.

His plan will coordinate efforts from the HPD, the New York City Housing Authority, the New York City Economic Development Corporation and the New York Public Library.

News of Adams’ plan comes just days after the city agreed to slash its practice of giving residents first dibs on new affordable apartments in their neighborhoods after settling a landmark federal lawsuit that claimed the Big Apple’s housing lottery promoted segregation.

Under the agreement approved Monday by a Manhattan federal judge, the city will soon only set aside 20% of units — down from the current 50% — for those locals vying to win the housing lottery in their own neighborhoods.

In addition to his new housing plan, Adams is expected to use his third State of the City address to touch on crime, jobs and the migrant crisis.

He is set to deliver the remarks at the Hostos Community College in The Bronx from 12:30 p.m.

Verdi Cannabis, the first legal recreational weed dispensary in Chelsea, will officially open on Friday.

Verdi will be located at 158 W 23rd St., between Sixth and Seventh avenues in Manhattan.

Father-and-son duo Mitchell and Ellis Soodak are the owners of Verdi, which will sell state-regulated marijuana products.

“Our dispensary will stand out because of our knowledgeable and educated budtenders sell tested and regulated cannabis, as well as providing a safer option for consumers,” Ellis Soodak said.

Verdi will be open from 9 a.m. to 11 p.m., Monday to Saturday, and from 10 a.m. to 10 p.m. on Sundays.

A grand opening ceremony will be held at 11 a.m. on Friday.

“Verdi represents a new era for cannabis enthusiasts in Chelsea,” Ellis Soodak said. “Our goal is for Verdi to be more than just a dispensary as we aim to be a critically important community alternative to the illicit cannabis establishments that have saturated the Chelsea area.”

The Travel Agency: A Cannabis Store is in line to be the first cannabis retail brand in New York State with multiple locations, as the legal-cannabis business starts gaining a foothold over illegal shops.

Separately, Curaleaf Holdings Inc. said it received special-use approval to open its first New York adult-use store, which will be located in Newburgh, a city about 70 miles north of New York City.

Curaleaf planned to kick off delivery service from the location this past weekend, with a soft opening by the end of January, pending state approval. New York-based Curaleaf has been providing cannabis to the medical market since 2017.

Curaleaf’s stock rose 7% on Friday. The shares are up by 23.5% in the past year, compared to a 37.4% rise by the Nasdaq

New York State’s legal-cannabis business is speeding up after a slow start due to some headwinds, including the cost of real estate and competition from literally thousands of unlicensed stores hawking unregulated cannabis products.

New York’s licensed-cannabis market generated only $150 million in sales in its first year of operation in 2023, less than the $274 million generated by the smaller state of Connecticut, which also kicked off adult-use sales about a year ago.

Gov. Kathy Hochul plans to propose legislation to crack down further on unlicensed cannabis shops. She’s also including a cannabis potency tax repeal and replacing it with a weight-based tax to “ease tax compliance” for distributors.

Hochul’s proposal comes mirrors a proposal in the state legislature to scrap the potency tax in favor of a 9% wholesale excise tax.

The idea is that cutting some cannabis taxes may lower the cost at the cash register and make legal pot more competitive with unregulated pot being sold in unlicensed stores.

Paul Yau, founder of the Travel Agency, said the effort by the state to cut taxes and close down unlicensed shops marks a positive move for the business.

“We 100% support trying to get rid of illicit stores,” Yau told MarketWatch, noting that Hochul made “having safe, tested, clean products” a priority by including a mention in her state-of-the-state address.

Cannabis companies have been slow to open for a variety of reasons. If a major bank holds a mortgage on a property, it may not allow a cannabis business to be a tenant because pot remains illegal under federal law.

Cannabis company operating expenses remain high because of these and other obstacles, he said.

Meanwhile, The Travel Agency is readying its second store at 118-122 Flatbush Avenue, near the Barclays Center in downtown Brooklyn, close to major public-transportation routes.

“We’re looking to make this the premier dispensary in Brooklyn,” Yau said.

The stores will initially open as a pop-up with 3,500 square feet, with 60 full-time and part-time workers, and then expand to 4,800 feet.

While adult-use cannabis has been approved since 2021, legal shops have been slow to gear up as the state awarded its first licenses to non-profits and people affected by the War on Drugs.

Travel Agency runs its two stores for license holders The Doe Fund in Manhattan and GMDSS LLC in Brooklyn.

The Travel Agency’s flagship store opened a year ago under the name Union Square Travel Agency just south of Union Square in Manhattan as the third overall retail cannabis shop in the state.

Now, the Travel Agency name will be used for both the original Union Square store and its downtown Brooklyn location, under a re-branding effort.

In November, the state also officially sanctioned its existing medical-use licensees to take part in the recreational market.

Those companies include Columbia Care, Curaleaf Holdings Inc., Etain, Nycanna LLC, PharmaCann and Valley Agriceuticals LLC

Companies with an existing presence in the state’s medical program include Curaleaf Holdings, RIV Capital Inc. Green Thumb Industries Inc. and privately held PharmaCann.

From NYPost.com, By Aneeta Bhole, Published Dec. 29, 2023

New York pot regulators bragged Friday about the financial success of the legal cannabis industry in 2023 — but made little mention of the millions in taxes being lost to the illegal marijuana stores spreading across the landscape like weeds.

The Office of Cannabis Management’s year end statement was filled with superlatives describing a blooming industry that brought in some $16.5 million in tax revenue on the sales of some 3.5 million pot products sold.

“2023 was a year of growth for New York cannabis and we know 2024 will be even more significant,” said John Kagia, the office’s Director of Policy, which said there was some $150 million in total legal sales this year.

The office, however, couldn’t put a price tag on how much was being sold at the estimated 1,500 illegal vendors operating on nearly every commercial block in the city and elsewhere in the state — which officials have complained have been stealing business from the measly 40 officially licensed shop currently approved in New York state.

The statement did say that they were cracking down on the illegal shops, and that more than 11,600 pounds of illicit products, with an estimated street value of more than $56 million, has been seized.

NY pot regulators boast $150M in legal cannabis sales as illegal marijuana stores rob state of millions in taxes (Provided by New York Post).

New York pot regulators bragged Friday about the financial success of the legal cannabis industry in 2023 — but made little mention of the millions in taxes being lost to illegal marijuana stores. Helayne Seidman

But when asked for details about the total size of the illegal industry, operating in plain sight, the state could provide no data.

Vendors setting up unlicensed shops mostly do business in cash and don’t pay cannabis taxes that licensed marijuana dispensary stores are required to do.

A spokesperson for the cannabis office said they “do not have firm or reliable estimates on total number of unlicensed shops.”

The Office of Cannabis Management’s year end statement was filled with superlatives describing a blooming industry that brought in some $16.5 million in tax revenue on the sales of some 3.5 million pot products sold (Getty Images).

The state said that close to 7,000 licenses were applied for processors, cultivation, distribution, microbusiness and retail dispensary this year and Kagia noted demand was high and is expected to grow.

“And now, with the Office poised to issue hundreds more adult use retail licenses, there’s tremendous excitement as consumers across the state are poised to gain access to this exciting market,” he said.

Just in New York over 500 strains have been made available to the exploding market with names such as Gas Face, Blueberry Muffin, and Sour Diesel.

2023 was a year of growth for New York cannabis and we know 2024 will be even more significant,” said John Kagia, the office’s Director of Policy, which said there was some $150 million in total legal sales this year (Matthew McDermott).

“There are also products available across the price spectrum, from low-cost value brands to ultra-premium product,” Kagia added.

“Furthermore, it’s not just flower products that are selling. Non-flower products, from infused gummies and innovative beverages like cannabis infused apple cider, to strain-specific vaporizers and high potency tinctures, ensure that there is something for everyone in this market.”